Financial Wellness and Retirement Security: Understanding Financial Vulnerabilities to Deliver Better Outcomes

By Hector Ortiz, Ph.D.

Saving for retirement requires more than access to a workplace 401(k) or IRA. A growing body of research demonstrates that retirement outcomes are shaped by a range of factors, from plan design features to household financial circumstances that enable or constrain saving behavior. Other factors also enable workers to contribute consistently and allow their savings to grow over time.

In my recent CRI paper, I explore state-level differences and trends across four specific financial vulnerabilities related to financial well-being and ability to save for retirement among people 18 and older who have retirement accounts, either through an employer-sponsored plan or individual accounts, such as IRAs. The four financial vulnerabilities are:

- Limited Financial Literacy — defined as incorrectly answering all three standard questions regarding compound interest, inflation, and stock diversification.

- Burdensome Debt — measured by agreement with the statement, “I have too much debt right now.”

- Lack of Emergency Savings — based on whether individuals report having set aside enough funds to cover three months of expenses in case of sickness, job loss, or other emergencies.

- Spending Exceeding Income — measured by whether spending over the past year exceeded total income.

These vulnerabilities matter. High debt competes directly with retirement contributions. Without positive cash flow, the ability to save may be reduced or stop altogether. A lack of emergency savings increases the likelihood of hardship withdrawals or loans. Finally, low financial literacy raises the risk of investing in unsuitable products, missing opportunities for compound growth, or being over-exposed to market and inflation risks.

Financial Vulnerabilities Are Substantial and Persistent

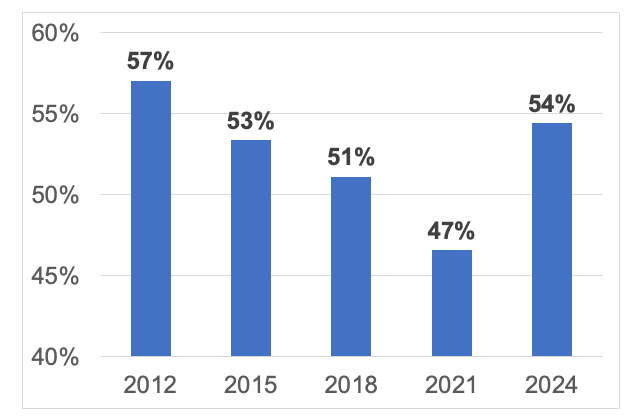

An examination of multiple waves of the FINRA Foundation’s National Financial Capability Study shows that financial vulnerabilities among retirement savers are substantial, and have grown since 2021. The analysis reveals that more than one-half of savers face these challenges, with a lack of emergency savings being the most common. In 2024, approximately 36% of retirement savers reported having no emergency savings. Furthermore, the share of retirement savers with two or more vulnerabilities is now greater than the share with exactly one, highlighting how compounding challenges are affecting a growing number of people.

Share of Retirement Savers with at Least One Vulnerability

Source: FINRA Foundation, National Financial Capability Study (2012–2024)

Understanding Vulnerabilities Can Drive Better Interventions

The analysis helps us understand the financial situation of savers, and provides a few insights to better target interventions:

- Prioritizing Emergency Savings — This is an area with real momentum. Options include incorporating “sidecar” emergency accounts into auto-IRA systems, partnering with financial institutions, or leveraging tax season. Evidence shows that even $500 to $1,000 in emergency savings can significantly reduce financial instability.

- Helping Savers who May Face Other Risks — Financial vulnerabilities are particularly high among savers who have been targets of fraud or who own cryptocurrency. This suggests that vulnerable savers are not only exposed to the risk of “leakage” from their accounts but also face an increased likelihood of other financial losses.

-

Tailoring Interventions — There are important variations across states, underscoring the need to tailor financial education and retirement policy to local economic conditions, and creating a clear opportunity to leverage state-facilitated retirement programs (like auto-IRAs) to improve literacy and expand coverage.

Financial Wellness: Achieving a Better Balance to Address Competing Needs

The key takeaway is that these challenges are interconnected, and savers achieve financial well-being when they are able to maintain financial stability today while making progress toward their long-term security.

There is a growing, and welcome, interest among employers in offering financial wellness programs that target issues such as monthly cash flow, debt management, emergency savings, caregiving, and fraud prevention. These programs integrate a wide range of resources, including coaching, planning, and professional advice. Supports that focus not only on long-term savings, but also on monthly cash flow, debt management, and emergency preparedness can help individuals make better decisions and strengthen retirement outcomes.

Hector Ortiz, Ph.D., is a Non-Resident Scholar, Center for Retirement Initiatives (CRI), Georgetown University.

The views expressed in this blog and the paper are the author’s own and do not necessarily reflect the views of the CRI or any other institutions with which the author is affiliated. The author assumes full responsibility for any errors or omissions.

26-01

March 2026

Additional Resources

Council for Economic Education. (n.d.). “2024 Survey of the States.”

Consumer Financial Protection Bureau. (2018). “Pathways to financial well-being: The role of financial capability.”

FINRA Investor Education Foundation. (2025). Foundation’s National Financial Capability Study (6th ed.).

The Urban Institute. (2025). Financial Health and Wealth Dashboard: A local picture of residents’ financial well-being.