Frequently Asked Questions

- State-Facilitated Retirement Savings Program Models

- Auto-IRA Common Program Design Features

- Fee Structures Across State Programs

- Positive Impact of State Programs on Private Employer-Sponsored Plan Formation

- Employer and Employee Program Experience

- Comparison of the Basic Features of an IRA and a 401(k)

- A Comparison of Traditional IRAs and Roth IRAs

- Vendors Servicing State-Facilitated Retirement Savings Programs

State-Facilitated Retirement Savings Program Models

What are the different types of state-facilitated retirement savings program models?

Among the states, four program models have emerged so far to expand private sector worker access to retirement savings options. These models are:

- Automatic-IRA: The Automatic IRA (Auto-IRA) model requires employers that do not otherwise already offer a retirement plan to allow their workers to be automatically enrolled in the state-facilitated retirement savings program. IRAs are considered personal savings accounts, not employee benefit plans, established and controlled by individuals, not employers, and therefore are not subject to ERISA. With state Auto-IRA programs, the role of the employer remains administrative only, restricted to enrolling workers and facilitating the payroll contribution. Employers also are prohibited from contributing to their employees’ accounts.

- Payroll Deduction IRA: In many respects, the program design is like an Auto-IRA program but differs in two important ways: 1) Employer participation in the program is voluntary and, if participation for employers is voluntary and not required by the states, then 2) there is legal uncertainty on what extent it can use auto-enrollment.

- Multiple Employer Plan (MEP): A MEP is commonly an ERISA 401(k) plan where several employers band together. As with a “single employer” 401(k), MEPs offer higher contribution limits than an IRA and potentially an employer contribution or match, allowing both employers and employees to contribute. Because state-facilitated MEPs are 401(k) benefit plans regulated by ERISA, a state cannot require employer participation. MEPs enable unrelated employers to join to form what is considered a single plan that can be administered by a third-party provider. Pooling the assets of numerous small and mid-sized employer 401(k) programs may allow the MEP to accumulate sufficient assets to negotiate lower fees for investment, recordkeeping, and other activities or services.

- Retirement Marketplace: Marketplaces are state-run “electronic clearinghouses” where businesses can find and compare retirement savings plans offered by private sector providers. Marketplaces usually include educational material that enables businesses to find and compare a diverse array of retirement savings plans that have been pre-screened to meet certain criteria in an apples-to-apples manner. In marketplaces, a diverse array of plans (IRAs and 401(k)s) can be pre-screened and regulated by the state to ensure certain standards.

Some states are creating programs that combine more than one element of these models. New Mexico, for instance, passed legislation to simultaneously establish a retirement marketplace and a voluntary payroll deduction IRA for employers. Other states and cities have considered, but not yet enacted, such tiered models. In June 2022, Hawaii enacted an Auto-IRA program that requires employees to opt-in and, if they do, then an employer must facilitate contributions.

For more information:

Source: Morse, David and Antonelli, Angela. (March 2021). State-Facilitated Retirement Savings Programs: A Policymaker’s Guide to ERISA and the Tax Code. Washington, DC: Georgetown University Center for Retirement Initiatives; State-Facilitated Retirement Savings Programs: A Snapshot of Program Design Features, State Guide, May 31, 2023, Update, Washington, DC: Georgetown University Center for Retirement Initiatives.

The responses to these questions are for general information and not intended as legal advice. Federal and state law and program terms should be carefully reviewed before taking any action.

[ Back to top ]

Auto-IRA Common Program Design Features

1. What’s the difference between a state program and an employer-sponsored retirement plan?

In an employer-sponsored plan, the employer takes on fiduciary responsibility by selecting, establishing, and often contributing to the plan. The retirement plan can be a 401(k) or one of several different individual retirement account (IRA) options. In a state program, oversight and governance is left to the state and the savings account is an IRA. The role of the employer is limited to enrolling workers and facilitating payroll contributions, and employers cannot make contributions to accounts.

2. What type of IRA can state programs offer?

A state program can use either a Roth or traditional IRA. Most state programs use a Roth IRA as the default savings vehicle, although they also make the traditional IRA available for participants who prefer it or whose income makes them ineligible for a Roth IRA.

3. Why do state programs often use the Roth IRA as the default instead of the traditional IRA?

The Roth IRA is the most common default because it tends to be a better fit for the workers state programs are designed to reach. Many savers have low-to-moderate income and are currently in a low tax bracket, making the Roth IRA’s upfront tax cost minimal while allowing their savings to grow and be withdrawn tax-free in retirement. Beyond potential tax benefits, Roth IRAs have the advantage of not requiring minimum distributions during the account owner’s lifetime, giving workers more flexibility with retirement planning. From an administrative perspective, a Roth IRA also makes it easier to process a participant’s “do-over” request to dis-enroll after participating for only a few pay periods, because the return of contributions is non-taxable and penalty-free. (Return of any investment income — likely to be small — would be taxable, and probably subject to the 10% early withdrawal penalty.)

States using a Roth IRA as the default will have no way of knowing whether a participant will exceed the Roth IRA income limit for the year. Contributions that exceed the income limit are subject to a 6% excise tax unless withdrawn by the individual’s income tax filing deadline. (The 6% tax is imposed annually until corrected.) Thus, state program communications inform participants of the earnings limit and correction rules for Roth and/or traditional IRAs.

Although there are strong reasons for using a Roth as the default, states also often allow participants to elect a traditional IRA, either because they earn too much to contribute to a Roth IRA or because the traditional version better meets their personal retirement or tax planning objectives.

4. What are employers required to do?

Employer responsibilities are limited to registering for the program, providing roster information for employees, and facilitating employee contributions through payroll deductions. Otherwise, most administrative and oversight duties are left to the state. Employers that already offer a qualified retirement plan exempt themselves from participation.

These responsibilities are often enforced by the state through compliance penalties. Penalty structures vary by state but commonly begin with a notice period and an opportunity to come into compliance before financial penalties are assessed. Penalties for non-compliance typically escalate over time but often up to pre-determined limit.

5. Are employers required to contribute to employee accounts?

No, employers are not permitted to contribute to employee accounts in state retirement programs. Their role is typically limited to facilitating payroll deductions and providing access to the program. This structure helps keep costs low for employers and makes state programs distinct from employer-sponsored retirement plans where employer contributions may be offered.

6. Can employees choose to opt-out of saving?

Yes, employees can choose to opt-out of saving. While most state retirement programs use automatic enrollment to encourage participation, employees are free to opt-out, change their contribution amount, or change their investment fund option at any time. Employees who opt-out can typically re-enroll at any time.

7. What types of investment options do state programs offer?

Many state programs offer a simplified set of investment options designed to make decisions easy for participants. The default investment option is often a target date fund (TDF), which automatically adjusts its asset allocation to become more conservative as the participant approaches retirement. In addition to the default investment option, programs commonly offer a capital preservation fund, a growth fund, and a fixed income fund. This menu of investments gives participants room to customize their portfolio.

8. What’s the most common default contribution rate offered by state programs?

The most common default contribution rate among state programs is 5% of taxable wages, while New York and New Jersey use a default contribution rate of 3%. This is the rate applied automatically when a participant is enrolled and has not selected a different rate. Participants can generally change their contribution rate at any time.

9. Do state programs use auto-escalation in addition to auto-enrollment?

Yes, most of the open programs use auto-escalation. It is most commonly an annual increase of 1% up to a cap of between 8% and 10%. This feature allows participants to gradually grow their savings without requiring them to actively make changes to their account. Participants who prefer to keep their contribution rate lower or steady can opt out of auto-escalation while remaining enrolled in the program.

10. Can an employee change their contribution rate or select their investments?

Yes, employees can change their contribution rate or select their investments at any time. Participants are not required to accept the default contribution rate or the default investment option. These defaults are starting points for participants who do not make an active election, but participants are free to change their contribution rate or select a different investment option from the program’s investment menu.

11. Are part-time or seasonal employees eligible to participate?

Yes, part time and seasonal employees are generally eligible to participate in state retirement programs. While “covered employee” definitions vary by program, most state programs are designed to include nontraditional workers. In 2025, for example, Minnesota amended its program to add temporary and seasonal workers to their definition of covered employees. Minimum eligibility thresholds such as age, earnings, or period of employment can vary by state and employers.

12. What happens to a participant’s account if they change jobs or leave the workforce?

A participant’s account stays with them if they change jobs or leave the workforce. State retirement programs are typically structured as portable individual retirement accounts (IRAs), meaning the account is owned by the worker and not the employer. Employees who change employers or move out of state can keep the same IRA or transfer savings to a different IRA. If a participant’s new employer is enrolled in a state program, payroll deductions can continue through the new employer. If the new employer is not part of the program, the participant can roll the funds into another retirement account or make contributions directly.

The responses to these questions are for general information and not intended as legal advice. Federal and state law and program terms should be carefully reviewed before taking any action.

[ Back to top ]

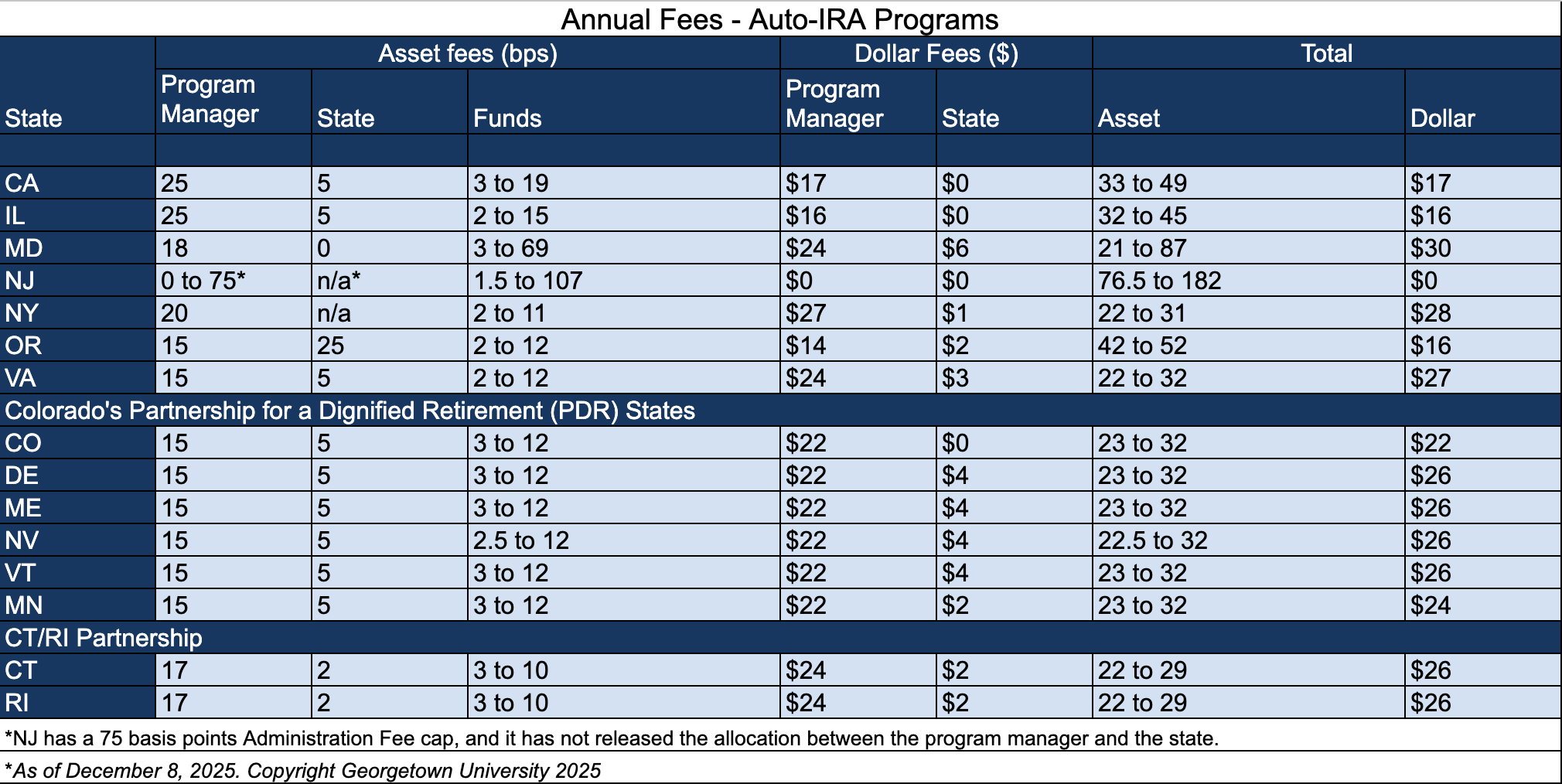

Fee Structures Across State Programs

What are the types and amounts of program fees?

Auto-IRA Programs:

Auto-IRA plans in Oregon, California, and Illinois initially all began exclusively relying on asset-based fees to cover program administration and state costs. The state program share of these fees were very low with most of the fees charged to support the program administrator (AKF Consulting Market Report, 2021).

However, in late 2021 Oregon (OregonSaves) changed its program administrator and took the opportunity to modify its existing fee structure to adopt a hybrid fee-based structure—utilizing dollar-based fees as well as asset-based fees. Oregon later announced additional adjustments to its fee structure in November 2022, still maintaining a hybrid structure but reducing its dollar-based fees.

Connecticut (MyCTSavings), Maryland (Maryland$aves), Colorado (Colorado Secure Savings), and Virginia (RetirePath VA) learned from the OregonSaves experience and implemented a hybrid-fee model at pilot/program launch. California (CalSavers) subsequently transitioned to include dollar-based fees in June of 2023, and Illinois Secure Choice is adopted a hybrid fee structure effective the first quarter of 2024.

While asset-based fees are sufficient to cover expenses for the underlying investment funds, Auto-IRA programs have learned much more about what they need to fund the operating costs of the state and the program administrator. A hybrid fee-based structure more effectively supports these needs. Private sector program administrators prefer dollar-based fees when programs have not yet reached critical mass to produce a more reliable revenue stream and while asset-based fees do not yet generate sufficient operating revenue. (AKF Consulting Market Report, 2022). Furthermore, dollar-based fees are viewed as cost-effective for participants in the long run as accounts grow.

The first fee reduction was made in the CalSavers program in April 2025 when it hit its first breakpoint of 555,000 saver accounts. The program manager’s dollar-based fee was reduced from $18 to $17 per year.

Multiple Employer Plans (MEPs):

Multiple Employer Plans (MEPs):

The only currently active MEP plan is Massachusetts CORE MEP. For the participant, there is a $65 annual fee, deducted automatically from the participant’s account, and other administrative fees depending on the “elective Plan features used by a participant. Each investment option has an administrative, advisory, and investment management fee that varies by investment option” and “additional fees, including administrative and other service fees, may be assessed over time.” For the participating nonprofit, there is a one-time installation fee of $2,500, a $200 plan administrative fee charged annually beginning in the second year, and an annual compliance fee of $150 for employer contribution election and $750 for deferral-only election

The “My Total Retirement” advisory service allows participants to receive custom portfolio management for a scaling percent fee, starting at 45 bps for the first $100,000, and shrinking for every $150,000 increment to a 15 bp fee for any amount over $400,000.

For more information:

Massachusetts CORE MEP program brochure

State-Facilitated Retirement Savings Programs: A Snapshot of Program Design Features, State Guide, May 31, 2023, Update, Washington, DC: Georgetown University Center for Retirement Initiatives.

[ Back to top ]

Positive Impact of State Programs on Private Employer-Sponsored Plan Formation

What impact does a state-facilitated retirement savings program have on employer-sponsored retirement plans in that state?

Georgetown CRI Working Papers

A study published by the National Bureau of Economic Research (NBER), and also published as a CRI working paper in 2023, using data from the Current Population Survey (CPS) and Form 5500 filings, examined the impact of state auto-IRA legislation on employee-sponsored retirement plans (ESRPs) and employee participation. The analysis examined California, Illinois, Oregon and Connecticut, and the data indicated that “auto-IRA legislation has a positive impact on the likelihood of employers offering retirement plans and individuals participating in these plans.”

NBER found that individuals are 3.2 percent “more likely to work for an employer who offers a retirement plan after auto-IRA policy implementation” in states where auto-IRA legislation has passed, and that the likelihood of worker participation in these plans increases by 7 percent. Furthermore, firms in states with auto-IRA programs are 1.5 – 1.7 percent are more likely to offer any kind of employee-sponsored retirement plan than those without these programs. The data indicates that “worker participation in existing retirement plans rises by 3 – 5 percent” in program states. The NBER study concludes that “auto-IRA policies significantly increase the likelihood of employers offering ESRPs, employee access to these plans, and participant numbers in existing ESRPs.”

The update to this NBER study, published as an updated CRI working paper in 2024, estimates that at least 30,000 firms have been induced to offer an ESRP by these policies, although there is substantial heterogeneity in these effects across firm and worker characteristics. This effect is large considering that, for employers, establishing and maintaining an ESRP is more costly than utilizing the state-facilitated IRAs.

The Pew Charitable Trusts

According to studies by the Pew Charitable Trusts that examined Form 5500 annual filings by employer-sponsored plans from 2013 to 2019 to the U.S. Department of Labor, auto-IRA programs do not undermine private retirement plan markets. Pew’s initial analysis, which covered 2013 to 2019 data, found that in states with auto-IRA programs, “employers with plans continue to offer them and businesses without plans are adopting new ones at rates similar to before the state options were available.”

Pew’s 2022 update, using 2021 Form 5500 data and focusing on California, Oregon, and Illinois, confirmed that state-facilitated retirement savings program complement, rather than compete with, employer-sponsored plans. Specifically, Pew found that in all three states, “the rate of introduction of new plans, as a share of existing plans, remained higher than before each introduced its savings program,” and the at which existing plans were terminated was below national average.

Pew’s 2024 update extended the analysis to include Connecticut and found similar patterns, concluding that “evidence from California, Oregon, Illinois, and now Connecticut, continues to indicate that auto-IRAs complement, instead of crowding out, private sector retirement plans such as employer-sponsored 401(k)s.”

Most recently, Pew’s April 2026 update, which drew on Form 5500 data through 2023 and expanded the analysis to seven states, adding Colorado, Maryland, and Virginia, reinforced these findings further. In 2023, “private businesses in California, Colorado, Connecticut, Illinois, Maryland, Oregon, and Virginia created new retirement plans at rates similar to or greater than the national average-in some cases, several years after the state had implemented a state-facilitated automatic enrollment workplace savings program.” Indeed, the data suggests that plan providers may ultimately be benefiting from the new market opportunities created by these state programs.

Gusto

According to Gusto, an HR platform designed for small businesses, internal data show that CalSavers compliance deadlines, company size, and employee wages strongly drive employers’ decisions to adopt private 401(k) plans. Gusto reported in 2022 that in response to the CalSavers June 30, 2022 compliance deadline, they “saw an increase of 35% in 401(k) adoption from our typical rate” between May 15 and June 30. Additionally, businesses that opted for a 401(k) before the deadline had employee salaries and wages approximately 36 percent higher than average and 27 percent more employees than average.

In a more recent, related report, Gusto examined private 401(k) adoption data following state auto-IRA program mandates in Colorado and Oregon, finding that overall adoption increased by 45 percent in Colorado and from 7 percent to 11 percent for Oregon firms with 1-4 employees. The data shows that the increases in 401(k) adoption were largest among low-income workers, with 401(k) enrollment nearly doubling for those earning under $25,000, while participant among higher earners grew more modestly. Gusto concludes that “auto-IRA compliance deadline are a significant driver of 401(k) adoption, and the beneficiaries are generally lower-earning employees of small firms.”

For more information:

Source: Bloomfield, Adam, Lee, Kyung Min, Philbrick, Jay, and Slavov, Sita, “State Auto-IRA Policies and Firm Behavior: Lessons from Administrative Tax Data,” Georgetown University Center for Retirement Initiatives Working Paper, 2024. (Update to 2023 NBER paper).

Source: Bloomfield, Adam, Lee, Kyung Min, Philbrick, Jay, and Slavov, Sita, “How Do Firms Respond to State Retirement Plan Mandates?” NBER Working Paper 31398, National Bureau of Economic Research, Inc., 2023.

Source: Scott, John. (April 16, 2026). States With Automated Retirement Savings Programs See Growth in New Private Plans. Philadelphia, PA: Pew Charitable Trusts.

Source: Guzoto, Theron, Hines, Mark, and Shelton, Alison. (November 18, 2024). State Automated Retirement Savings Programs Don’t Crowd Out Private Plans. Philadelphia, PA: Pew Charitable Trusts.

Source: Guzoto, Theron, Hines, Mark, and Shelton, Alison. (April 14, 2023). State Automated Retirement Savings Programs Continue to Complement Private Market Plans. Philadelphia, PA: Pew Charitable Trusts.

Source: Guzoto, Theron, Hines, Mark, and Shelton, Alison. (July 25, 2022). State Auto-IRAs Continue to Complement Private Market for Retirement Plans. Philadelphia, PA: Pew Charitable Trusts.

Source: Abbott, Steve and Pardue, Luke. (December 6, 2023). State Auto-IRAs Mandates Boost 401(k) Adoption, With Largest Gains Among Lower-Income Workers. Gusto.

Source: Abbott, Steve. (September 13, 2022). State Auto-IRAs can Boost 401(k) Adoption. Gusto.

What impact does a state-facilitated retirement savings program have on employee financial security?

According to a study published in 2024 by the Pew Charitable Trusts analyzing credit data from a survey of savers in Illinois Secure Choice, of the 36 percent who gave access to their credit profiles, “participants in Illinois Secure Choice had lower credit scores when compared with those who opted out and with all Illinois adults, but participants had greater increases from on year to the next, both in the actual numerical change and in the percent change.” Overall, these findings provide an early indication that participation in state-facilitated retirement program may help improve financial outcomes over time.

A study published in 2024 by Gusto, which analyzed retirement savings and participation data in Maryland, Connecticut, Massachusetts, and Pennsylvania, determined that “employees are 20% more likely to contribute to a retirement savings account if they work for a company based in states that have auto enrollment IRA policies.” This increase in contributions is most pronounced – 55 percent – among earners at or below the median income. Gusto concludes that savings gains from auto-IRA programs are more evenly distributed across income levels than previously thought.

For more information:

Source: Hines, Mark. (December 12, 2024). Illinois Secure Choice Retirement Program Participants See Improved Credit Scores. Philadelphia, PA: Pew Charitable Trusts.

Source: Abbott, Steve and Tremper, Nich. (November 14, 2024). Auto-Enroll state Retirement Savings Policies Significantly Increase Savings Rates. Gusto.

[ Back to top ]

Employer and Employee Program Experience

How do employers surveyed view their experience with state programs?

OregonSaves

According to surveys conducted in 2020 and 2021 by the Pew Charitable Trusts, employers reported the following:

- About 80 percent of OregonSaves employers did not report any out-of-pocket costs with the program.

- 80 percent of participating firms in OregonSaves reported no or few employee questions or concerns.

- 73 percent of employers surveyed reported they were either satisfied with or neutral about their program experience.

Sources: Scott, John and Hines, Mark. (May 2021). Is the OregonSaves Retirement Program Expensive for Employers?; (March 2021). OregonSaves Auto-IRA Program Elicits Few Questions from Employees; and (July 2020). Employers Express Satisfaction With New Oregon Retirement Savings Program. Philadelphia, PA: Pew Charitable Trusts.

How do employees surveyed view their experience with state programs?

Illinois Secure Choice

In a 2022 survey conducted by the Pew Charitable Trusts, workers reported the following:

- Almost 40 percent reported that the program made them feel more financially secure.

- Approximately 60 percent were either very satisfied or satisfied with their program experience, and 96 percent were neutral or satisfied.

- More than two-thirds reported that they trusted information from the Illinois Secure Choice Program.

Source: Scott, John and Hines, Mark. (April 18, 2022). Many in Illinois Retirement Savings Program Feel Their Financial Security Is Improving. Philadelphia, PA: Pew Charitable Trusts.

Is there support for state programs?

Multi-State Surveys

In a 2025 analysis of a survey conducted in 2023 by the Pew Charitable Trusts, small businesses across Massachusetts Pennsylvania, and Washington reported the following:

- 84 percent of respondents in Massachusetts, 76 percent in Pennsylvania, and 73 percent in Washington said they would support their state starting an automated savings program.

- 79 percent of respondents that are members of the state or local chamber of commerce, and 75 percent of respondents that are members of the National Federation of Independent Business, support adoption of an automated savings program.

- Among those surveyed, 70 percent of Republicans, 70 percent of independents, and 89 percent of Democrats supported an automated savings program, indicating broad bipartisan support.

- Although some individual respondent characteristics (such as the age of the business or the age of the business-owner) are associated with slightly lower support, majorities across all groups expressed support for automated savings program adoption.

Source: Scott, John. (March 25, 2026). Most Small Business Owners Support the Adoption of a State Automated Retirement Savings Program. Philadelphia, PA: Pew Charitable Trusts.

National Surveys

In a 2024 analysis by the National Institute on Retirement Security, Americans reported the following:

- 77 percent agreed that state-facilitated retirement savings programs are a good idea.

- More than three-quarters said they would participate in a state-facilitated retirement program, up from 75 percent in 2020.

- A strong majority view key features of state-facilitated retirement programs favorably, with about 87 percent citing their potential for higher returns than other low-risk investments and 86 percent highlighting their low fees.

Source: Doonan, Dan and Kenneally, Kelly. (May, 2024). Americans’ Views of State-Facilitated Retirement Programs. Washington, DC: National Institute on Retirement Security.

[ Back to top ]

Comparison of the Basic Features of an IRA vs. a 401(k)

What are the differences between IRAs and 401(k)s?

| State Auto-IRA | 401(k)/DC | |

| ERISA Regulation | Non-ERISA | ERISA |

| Administrative Simplicity | Yes | Somewhat (single plans vs. MEP/PEP affects burden on employers) |

| Contributions Allowed | Employee pre-tax/Roth | Employee pre-tax/Roth and employer |

| Investments | Employee chooses from plan “menu,” including a pooled and professionally managed option and/or private sector (third-party) options | Employee chooses from plan “menu,” including a pooled and professionally managed option and/or private sector (third-party) options |

| Employers Required to Adopt | Yes, under current law | Unlikely |

| Auto-enrollment with Employee Opt-Out | Yes | Yes |

| Pros |

|

|

| Cons |

|

|

Sources:

Morse, David and Antonelli, Angela. (March 2021). State-Facilitated Retirement Savings Programs: A Policymaker’s Guide to ERISA and the Tax Code, Table A, p. 2. Washington, DC: Georgetown University Center for Retirement Initiatives.

Internal Revenue Service. (2025, November 13). 401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500. https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

The responses to these questions are for general information and not intended as legal advice. Federal and state law and program terms should be carefully reviewed before taking any action.

[ Back to top ]

A Comparison of Traditional IRAs and Roth IRAs

What are the differences between a Traditional IRA and a Roth IRA?

Traditional IRAs |

Roth IRAs |

|

| Eligibility | Individual must have a salary, self-employment earnings, or other taxable compensation.

There is no age maximum. |

Same as traditional, and individual (plus spouse if married, filing a joint return) must have modified adjusted gross income (MAGI) below specified limits. For 2026, the limits are as follows.

Single filer with MAGI of:

Joint filers with MAGI of:

|

| Deductible Contributions | For 2026:

Contributions are tax-deductible if individual (and spouse) is not covered by a 401(k) or other retirement plan. Contributions come out of employee paychecks pre-tax and are instead taxed on distribution at retirement. If covered by a retirement plan, contributions are deductible only if income is below certain limits. For 2026: Single filer, covered by a retirement plan at work, with MAGI of:

Joint filer, covered by a plan at work, with MAGI of:

|

Roth contributions are not tax-deductible. |

| Federal Income Tax Treatment on Contributions and Earnings | Earnings grow tax-deferred until distributions begin. Distributions are taxed as ordinary income. Withdrawals of nondeductible contributions are not taxed. | Withdrawals of contributions are not taxed. Qualified distributions are tax-free.

Earnings on nonqualified distributions earnings are taxed as ordinary income and may be subject to a penalty. |

| Penalties on “Early” and “Late” Distributions | Distributions from contributions and earnings can be taken after age 59½ without a federal tax penalty.

Required minimum withdrawals (RMDs) (based on life expectancy) must begin by age 73. Late distributions are subject to 25% excise tax, which may be reduced to 10% if the RMD is corrected within two years. Distributions before age 59½ are subject to a 10% penalty tax unless certain exceptions are met, including:

|

Distributions from earnings are tax-free if the initial contribution to the IRA was made at least five years ago and the individual is:

Payments made to beneficiaries after the five-year period are also tax- and penalty-free. Payments made before the end of the five-year period are penalty-free. Distributions from earnings are not subject to the 10% penalty if they qualify for an exception — the same as exceptions for traditional IRAs. |

Sources:

Morse, David and Antonelli, Angela. (March 2021). State-Facilitated Retirement Savings Programs: A Policymaker’s Guide to ERISA and the Tax Code, Table B, p. 7. Washington, DC: Georgetown University Center for Retirement Initiatives.

Internal Revenue Service. (2025, November 13). 401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500. https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

Internal Revenue Service. (2024, December 10). Retirement plan and IRA required minimum distributions FAQs. https://www.irs.gov/retirement-plans/retirement-plan-and-ira-required-minimum-distributions-faqs

The responses to these questions are for general information and not intended as legal advice. Federal and state law and program terms should be carefully reviewed before taking any action.

[ Back to top ]

Vendors Servicing State-Facilitated Retirement Savings Programs

Who are the vendors servicing state-facilitating state retirement programs?

Auto-IRA Programs

Washington

Expected launch: 2027

- Program Consultant: AKF Consulting

- Program Administration: To be determined

- Investment Consultant: Meketa

- Investment Funds Management: To be determined

Hawaii (CT Multistate Alliance for Retirement Security):

Expected launch: Late 2026

- Program Consultant: To be determined

- Program Administration: Vestwell

- Investment Consultant: To be determined

- Investment Funds Management: To be determined

Minnesota (CO Partnership for a Dignified Retirement):

Program launch: January 1, 2026

- Program Consultant: None

- Program Administration: Vestwell

- Investment Consultant: None

- Investment Funds Management: State Street and BlackRock

Rhode Island (CT Multistate Alliance for Retirement Security):

Expected launch: October 21, 2025

- Program Consultant: To be determined

- Program Administration: Vestwell

- Investment Consultant: To be determined

- Investment Funds Management: Fidelity, Schwab, and Vanguard

New York:

Program launch: October 8, 2025

- Program Consultant: AKF Consulting

- Program Administrator: Vestwell

- Investment Consultant: Marquette

- Investment Funds Management: State Street and BlackRock

Nevada (CO Partnership for a Dignified Retirement):

Program launch: June 17, 2025

- Program Administration: Vestwell

- Program Consultant: AKF Consulting

- Investment Consultant: None

- Investment Funds Management: State Street and BlackRock

Vermont (CO Partnership for a Dignified Retirement):

Program launch: December 1, 2024

- Program Consultant: None

- Program Administration: Vestwell

- Investment Consultant: RVK

- Investment Funds Management: State Street and BlackRock

Delaware (CO Partnership for a Dignified Retirement):

Program launch: July 1, 2024

- Program Consultant: None

- Program Administration: Vestwell

- Investment Consultant: CapTrust

- Investment Funds Management: State Street Global and BlackRock

New Jersey:

Program launch: June 30, 2024

- Program Consultant: None

- Program Administration: Vestwell

- Investment Consultant: Pending

- Investment Funds Management: Vanguard, Fidelity, Wasatch, Baird

Maine (CO Partnership for a Dignified Retirement):

Program launch: January 27, 2024

- Program Consultant: None

- Program Administration: Vestwell

- Investment Consultant: CapTrust

- Investment Funds Management: State Street and BlackRock

Virginia:

Program launch: June 20, 2023

- Program Consultant: AKF Consulting

- Program Administration: Vestwell

- Investment Consultant: Mercer

- Investment Funds Management: BlackRock

Colorado (Lead: CO Partnership for a Dignified Retirement):

Program launch: January 18, 2023

- Program Consultant: None

- Program Administration: Vestwell

- Investment Consultant: Segal Marco

- Investment Funds Management: State Street and BlackRock

Maryland:

Program launch: September 15, 2022

- Program Consultant: AKF Consulting

- Program Administration: Vestwell

- Investment Consultant: AonHewitt

- Investment Funds Management: BlackRock, State Street, Lincoln Financial Group, and T. Rowe Price

Connecticut:

Program launch: April 1, 2022

- Program Consultant: AKF Consulting

- Program Administrator: Vestwell

- Investment Consultant: Segal Marco

- Investment Advisor: Lockwood Advisors

- Investment Fund Managers: Fidelity, Schwab, and Vanguard

California:

Program launch: July 2019

- Program Consultant: AKF Consulting

- Program Administrator: Ascensus

- Investment Consultant: Meketa

- Investment Funds Management: State Street

Illinois:

Program launch: October 2018

- Program Consultant: AKF Consulting

- Program Administration: Vestwell

- Investment Manager: Marquette

- Investment Funds: BlackRock, Charles Schwab, State Street

Oregon:

Program launch: October 1, 2017

- Program Consultant: None

- Program Administration: Vestwell

- Investment Consultant: Sellwood Consulting (also consulting role)

- Investment Funds Management: State Street

Multiple Employer Plans (MEPs)

Massachusetts CORE Program:

Program launch: October 27, 2017

- Program Administration: Empower Retirement

- Investment Consultant and ERISA Fiduciary: AonHewitt

- ERISA Fiduciary Administrative Services: Northeast Professional Planning Group

Marketplace

Utah Retirement Exchange:

Expected launch: TBD

- Program Administration: Direct 401k, LLC

New Mexico Work & $ave:

This program has been put on indefinite hold with no known new implementation date. These contracts have likely expired.

- Program Consultant: AKF Consulting

- Marketplace Consultant: Massena Associates

- Strategic Planning and Communications Consultant: Carroll Strategies LLC

Washington Small Business Retirement Marketplace:

Program launch: March 19, 2018

- IRA products: Aspire Capital Advisors; previously also provided by Finhabits

- 401(k) products: none currently; previously provided by Saturna which exited in January 2022

Other program states will be added as they enter contracts with vendors.

This list is as of August 5, 2026, and will be updated periodically.

Source: Georgetown University Center for Retirement Initiatives compiled from state and public sources. Use of this list and this information collected by the Center should be attributed to the Center.

[ Back to top ]