The Role of Health in Strengthening Retirement Security

By Hector Ortiz, Ph.D.

An individual’s health before retirement and during retirement has significant financial implications for their financial well-being. Maintaining good health can help protect retirement savings, extend working years, and reduce the costly risks associated with long-term care. In other words, health can serve as an important lever for individuals facing savings challenges by helping to reduce both current and future expenses while mitigating a wide range of retirement risks. More people are recognizing this connection and taking steps to improve their health as they approach retirement.

The Federal Reserve Board’s Survey of Household Economics and Decisionmaking (SHED) asks respondents about the timing of their retirement and the reasons behind it. In this analysis, I combine data from multiple survey waves, including newly released data, to better understand the circumstances of individuals who retired for health-related reasons and consider the broader implications for retirement planning. I also examine workers who have not yet retired but report reducing their work hours because of health limitations or experiencing fair or poor health.

Health Is a Leading Cause of Retirement

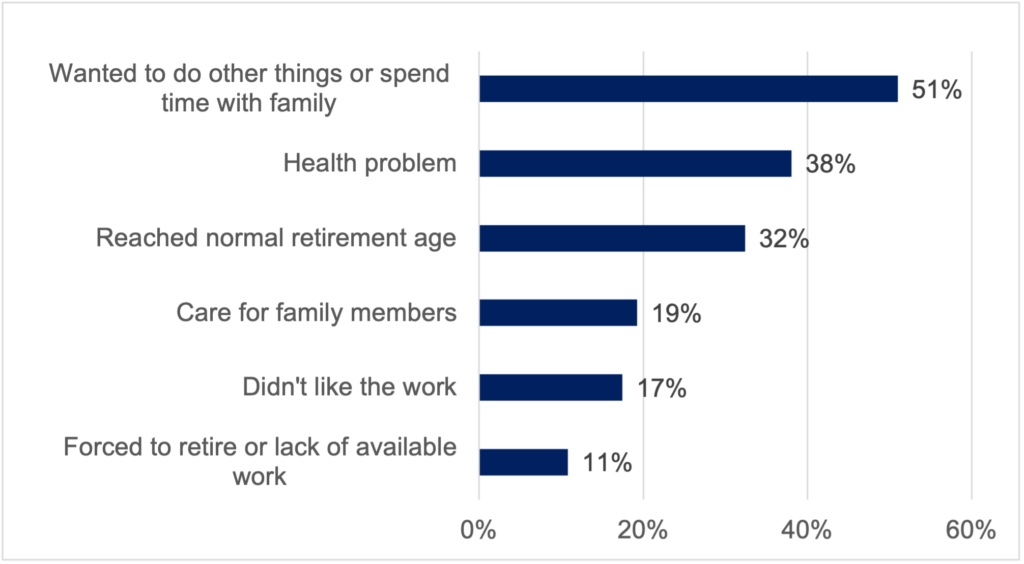

Survey respondents were asked to identify the reasons they retired when they did. Between 2021 and 2025, nearly one-third of retirees who were under the age of 70 at the time of the survey reported retiring for health-related reasons. This makes health the second-most commonly cited reason for retirement, after wanting to do other things or spend more time with family.

Figure 1. Reasons for Retiring among Retirees under Age 70

Source: Author’s calculations using the Federal Reserve Board’s Survey of Household Economics and Decisionmaking (2021–2025 pooled sample).

Health-related retirements tend to be involuntary and unplanned, with only 22% of retirees under 70 who retired due to health reasons also reporting that they retired because they reached “normal” retirement age. In comparison, 38% of those who retired to do other things or spend more time with family also reported retiring because they had reached normal retirement age. Another sign that these retirements may have occurred earlier than expected is that 50% of those who retired for health reasons were under age 62 at the time of the survey. Retiring before age 62 can create additional financial pressures, including reduced retirement benefits, gaps in health insurance coverage, possible early withdrawal penalties, and the need for earlier withdrawals from retirement savings to bridge the years before becoming eligible for Social Security.

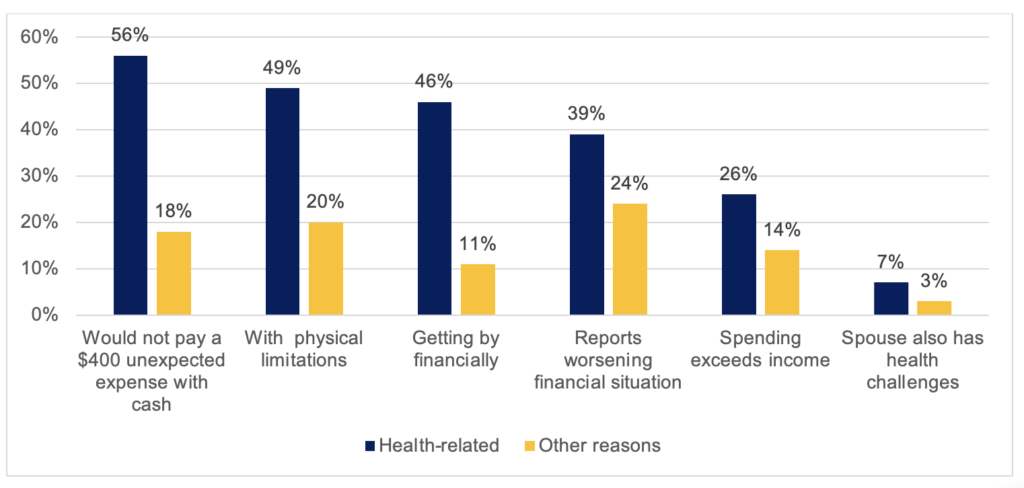

Health-Driven Retirements Come with Immediate and Long-Term Financial Challenges

Individuals who retire due to health reasons face a wide range of financial difficulties. Compared with those who retire for other reasons, they are more likely to report:

- Just getting by financially

- Worsening financial conditions in the past year

- Expenses exceeding income

- Would pay for a $400 unexpected expense using other method than cash or cash equivalent, a widely used measure of lack of emergency savings

Figure 2. Selected Financial Circumstances of Retirees under Age 70 by Reason for Retiring

Source: Author’s calculations using the Federal Reserve Board’s Survey of Household Economics and Decisionmaking (2021–2025 pooled sample).

In addition, 49% of these retirees also report disabilities, including vision and hearing impairments or limitations with activities of daily living such as walking, climbing stairs, or dressing; 7% also report that their spouses reduced work hours because of health-related limitations or caregiving responsibilities for an adult.

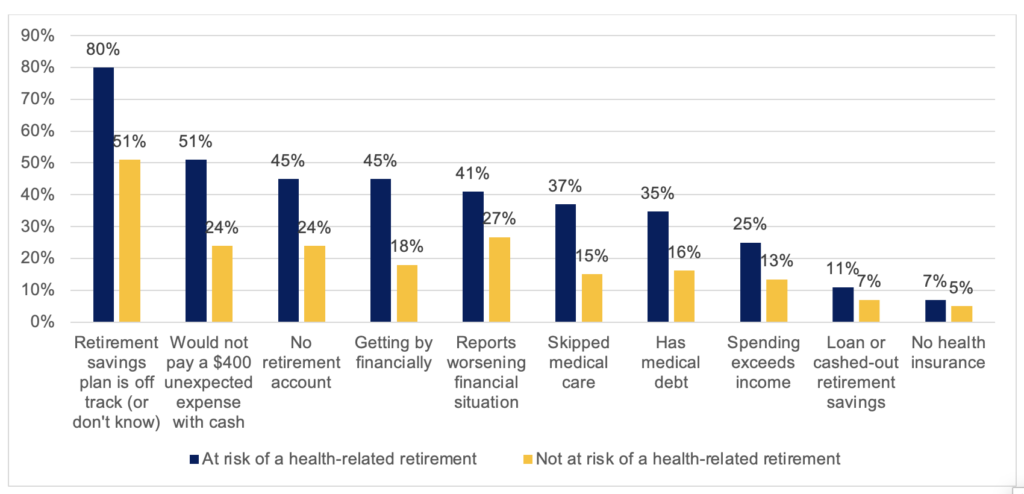

Many Workers Face Health Risks that Could Disrupt Retirement Plans

The survey includes questions about health status and whether respondents have reduced work hours because of health limitations. Together, these measures help identify workers who may be at greater risk of earlier-than-expected retirement. In the survey, 13% of working adults ages 50 to 64 report having poor or fair health or reducing their work hours due to health reasons.

These workers are less likely to have retirement accounts compared with those who do not face such challenges. Among workers facing health-related challenges, 11% report that they have taken a withdrawal or loan from retirement accounts and only 20% report that their retirement savings plan is on track.

Figure 3. Financial Circumstances of Workers Ages 50 to 64 by Health Status

Source: Author’s calculations using the Federal Reserve Board’s Survey of Household Economics and Decisionmaking (2021–2025 pooled sample).

Similar to those who have already retired due to health reasons, workers ages 50 to 64 who face health challenges are also more likely than their counterparts to report that they are just getting by financially, their financial conditions are worsening, their expenses exceed their income, and they would have to pay for a $400 unexpected expense using a method other than cash or cash equivalent.

These workers also face challenges related to getting care. Although 93% have health insurance, 37% reported skipping needed medical care and 35% have medical debt. These findings raise important questions about how to support workers better in maintaining their health while they remain employed.

Demographically, 51% of workers ages 50 to 64 at risk of health-related retirement are women, 52% are non-Hispanic white, 51% have a high school diploma or less, and 30% have incomes below $50,000. In comparison, 48% of workers who don’t face these health challenges are women, 66% are non-Hispanic white, 30% have a high school diploma or less, and 11% have incomes below $50,000.

Strengthening the Link Between Health and Financial Planning

These findings are consistent with other research showing that health-related issues and challenges lead to earlier than expected retirement, are the most common source of unexpected expenses, and are a major source of leakage from retirement savings and spending in retirement. The insights from this analysis point to the need for greater collaboration among stakeholders in both the financial planning and health sectors.

- Expanding support in health insurance coverage: Beyond offering health insurance benefits, employers and other stakeholders can play an important role in helping individuals understand and navigate their options. Access to appropriate coverage is critical not only for maintaining health but also for managing costs and avoiding unexpected financial burdens. Helping individuals choose plans that align with their medical and financial needs may improve both health and financial outcomes.

- Incorporating health into financial planning: Retirement planning should integrate health-related considerations more fully, including healthcare costs, the potential effects of health on retirement timing and longevity, caregiving responsibilities, and the risk of needing long-term services and supports (LTSS). The good news is that many major providers devote sections of their planning materials to healthcare and spending costs, and major financial and retirement certifications include related content. However, this still raises questions about the need for deeper and more personalized interventions. Such efforts may require stronger partnerships between financial professionals and health-related support services that can help individuals develop and maintain healthier lifestyles.

- Supporting more research to inform practice: Grantmakers and other funders should continue supporting updated and new research about healthcare costs, out-of-pocket spending, and long-term care risks that can help financial educators, planners, and policymakers better understand the challenges individuals face as they approach retirement.

A focus on health can improve a worker’s ability to save for retirement through their career and retire on their own terms. For retirees, a focus on health gives them quality of life and the ability to enjoy their retirement years, while also strengthening financial well-being. By considering the relationship between health and finances today and into the future, individuals can better protect their retirement security and build a more stable future.

Methodology

This analysis combines responses from the 2021 through 2025 waves of the Federal Reserve Board’s Survey of Household Economics and Decisionmaking (SHED). Conducted since 2013, SHED measures the economic well-being of U.S. households and includes questions about a range of topics, including credit access and behaviors, savings, retirement, economic fragility, and demographics. With approximately 12,000 respondents per survey year, the total combined/sample for this analysis is 60,170. Pooling the data allows for a deeper examination of patterns and experiences among groups while improving the ability to analyze populations that may be smaller in any individual survey year.

The analysis focuses on a subsample of respondents who self-identified as retirees, including a subsample of 3,577 retirees under age 70 who reported retiring due to health reasons. Although the question about reasons for retirement was asked of all retired respondents, this analysis focuses on retirees who are under age 70 to reduce potential analysis biases related to recall, mortality, and changes in sample demographic composition over time. The analysis also examines a subsample of non-retired workers, including a subsample of 1,474 workers ages 50 to 64 who reported health limitations or reducing work hours because of health-related issues.

2026-05

June 2026

Hector Ortiz, Ph.D., is a Non-Resident Scholar, Center for Retirement Initiatives (CRI), Georgetown University.

The views expressed in this blog post and the paper are the author’s own and do not necessarily reflect the views of the CRI or any other institutions with which the author is affiliated. The author assumes full responsibility for any errors or omissions.

Additional Resources

Federal Reserve Board (2026). Survey of Household Economics and Decisionmaking.

Employee Benefit Research Institute (EBRI) and Greenwald Research. (2026). 2026 Retirement Confidence Survey.

Munnell, Alicia H., Matthew S. Rutledge, and Geoffrey T. Sanzenbacher. (2019). Retiring Earlier than Planned: What Matters Most?

AARP. (2024). 8 Things to Do After 50 to Help You Live Longer.