By Catherine Harvey

In the field of retirement and financial wellness, most people can recite the Federal Reserve’s statistic that 40% of U.S. households would struggle to cover a $400 unexpected expense. The AARP Public Policy Institute went beyond “the $400 problem” in our recent report, Unlocking the Potential of Emergency Savings Accounts, and presented a more-nuanced portrait of the population that lives one surprise away from financial distress. We also identified factors that make people more likely to save successfully. These insights clarify unique roles for policymakers, financial institutions, employers, and researchers to ensure that more people can cope with inevitable unexpected events that have financial impacts.

How Well Do Americans Prepare for Financial Emergencies?

Our analysis of the U.S. Financial Health Pulse, an ongoing snapshot of how people in America manage their finances, found:

- 53 percent of US households have no emergency savings account.

- Many middle- and upper-income households have no emergency savings accounts, while some low-income households do have them. For example, more than a quarter of people with household income between $20,000 and $39,000 have an emergency savings account.

- People who say they have emergency savings accounts are twice as likely to have $2,000 or more in liquid savings.

- People with emergency savings accounts are more than twice as likely to use automatic transfers – such as between checking and savings accounts – compared with people without emergency savings accounts.

People with emergency savings accounts are 2.5 times more likely to be confident about meeting their long-term financial goals.

Retirement experts may be especially interested in our finding that people with emergency savings accounts are 2.5 times more likely to be confident about meeting their long-term financial goals. It makes sense that short-term financial resilience gives people peace of mind for the future.

The Importance of Emergency Savings

An emergency or precautionary savings account is one form of household liquidity. Liquidity refers to financial resources that consumers can deploy quickly to deal with an unexpected financial event. The Federal Reserve considers liquid savings to include balances in checking and savings accounts; cash; prepaid cards; and stocks, bonds, and mutual funds.

Evidence is growing that liquid savings are especially useful for keeping household finances on track when people encounter a modest financial shock. For example, savings of just $250 to $749 can significantly reduce the likelihood that households will be evicted or need to rely on public benefits. In some cases, maintaining modest emergency savings may be preferable to paying off high-interest debt; even a small amount of savings is associated with a lower likelihood of coming up short for rent or missing a mortgage payment, skipping medical care, or going without food.

In addition to buffering against financial hardship in the near term, emergency savings can shore up long-term financial security. Savings can provide a safer cushion than unsecured debt and alternative high-cost financial services such as payday loans, which have been shown to keep borrowers indebted for months or years and often lead to default, delinquency, and bankruptcy.

Emergency savings can also help protect retirement assets for households that have retirement savings. Evidence from the employer-based retirement system suggests that many people rely on their retirement accounts to cope with a financial shock. One survey found that 49 percent of employees expect that they will tap their retirement savings for a nonretirement expense.

We know that a lack of a liquid financial cushion contributes to leakage from the retirement system; Transamerica reports that emergencies are responsible for about 23 percent of loans from retirement accounts and we suspect a similar or larger share of early withdrawals are due to a lack of liquid savings. According to our report, half of people over age 50 do not have an emergency savings account. For older workers with less time to regain their losses, tapping their retirement accounts to cover an emergency expense could permanently compromise their retirement security.

What Role Can Retirement Systems Play to Improve Financial Resiliency?

What role, if any, does the retirement system have in bolstering people’s financial resilience in the short term? Some retirement plan providers, both in the U.S. and internationally, are tackling the $400 problem head-on by making it much easier to direct payroll contributions into more liquid after-tax emergency accounts as well as traditional retirement accounts. In fact, the first $1,000 of an individual’s contributions to the state-facilitated retirement savings programs in California, Oregon, and Illinois go into relatively liquid accounts that participants could use for emergencies with little to no penalty. In the past year, the UK NEST program has begun to test directing a portion of savings into an emergency account; once that account has been filled, the balance of automatic contributions go into the participant’s retirement account.

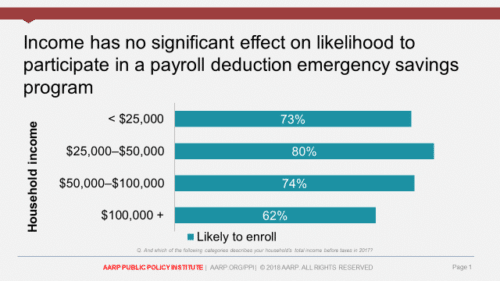

As retirement providers and plan sponsors weigh whether and how to address the short-term savings challenge, they would do well to consider the preferences of plan participants. Last year, AARP in collaboration with behavioral economist Warren Cormier found that 71% of working adults liked the concept of a payroll deduction emergency savings program. Support for a program was high in all income levels and demographic groups. What’s more, making participation in an emergency savings program the default did not dampen workers’ support. Automatic enrollment as a path to successful and sustained retirement savings habit could be a powerful component of a similar effort to help people build short-term savings.

Conclusion

Our analysis of the U.S. Financial Health Pulse confirms that having emergency savings is a critical component of household financial security. Emergency savings help families weather financial shocks and improve overall financial confidence.

Various stakeholders can do much more to help more Americans save for emergencies, and this preparation can help encourage and preserve retirement savings. Policymakers should take action to create incentives and remove barriers to make it as easy as possible to save. At the same time, the financial industry and employers can take steps to design affordable products, services, and tools to help the financially vulnerable while researchers continue to explore innovative new approaches to save and the relationship between savings and short-term and long-term financial security.

Catherine Harvey is a Senior Policy Advisor with the AARP Public Policy Institute.

December 2019, 19-08

Additional Resources

AARP Public Policy Institute, “Unlocking the Potential of Emergency Savings Accounts,” October 2019.

AARP Public Policy Institute, “Saving at Work for a Rainy Day,” September 2018.

John Beshears, James J. Choi, Mark Iwry, David John, David Laibson, and Brigitte C. Madrian, Building Emergency Savings Through Employer-Sponsored Rainy-day Savings Accounts, NBER Working Paper #26498, November 2019.

Federal Reserve, “Report on the Economic Well-Being of U.S. Households in 2018,” May 2019.

U.S. Government Accountability Office, “Retirement Savings: Additional Data and Analysis Could Provide Insight into Early Withdrawals,” March 2019.