How Retirement-Ready Is Your State?

Many non-retired adults have not estimated how much money they will need for retirement

By Hector Ortiz and Carly Urban

One common measure of retirement preparedness is whether people have ever tried to figure out how much they will need for retirement. Estimating retirement savings needs helps individuals make a wide range of important decisions, such as whether to seek financial advice, how much to contribute to their savings accounts, and when they can afford to retire. This planning exercise is particularly important for higher-earning individuals, who may need to save more to supplement their Social Security income.

Using data from the FINRA Foundation’s 2024 National Financial Capability Study (NFCS), we examine how many non-retired adults have tried to estimate their retirement savings needs. While individuals with greater financial literacy, higher incomes, and access to an employer-based retirement plan are more likely to have done so, a significant share still has not. From 2012 to 2024, there was only a small improvement in the share of non-retired people estimating their retirement savings needs, despite overall gains in income and access to employer-based retirement plans. We also find striking differences among states, as well as in how these patterns have changed over time.

Many Working Adults Have Not Estimated Their Retirement Needs

The NFCS asks non-retired adults whether they have ever tried to figure out how much money they will need for retirement. Our analysis finds that only 39% of non-retired adults ages 18 and older have done so. Despite nearing retirement and being more likely to face important financial decisions, only 48% of non-retired adults ages 55 and older have done so.

Three expected groups of non-retired adults are more likely to have calculated their retirement savings needs: those with greater financial literacy, access to a retirement plan, and higher incomes. However, substantial gaps remain even among these groups:

- 55% of non-retired respondents with a retirement plan said they had tried to estimate how much they will need for retirement, compared with 21% of those without a plan.

- 59% of non-retired respondents who correctly answered three financial literacy questions (about compound interest, inflation, and risk diversification) had estimated their needs, compared with 32% who answered only one or two correctly.

- 53% of non-retired respondents with household incomes above $50,000 had estimated their needs, compared with 21% of those earning less than $50,000.

These findings are consistent with results from the Employee Benefit Research Institute’s Retirement Confidence Survey and research using the University of Michigan’s Health and Retirement Study. At the same time, they are somewhat surprising, given the widespread availability of online calculators and planning tools.

Small Improvement Since 2012

The NFCS has asked about estimating retirement savings needs consistently since 2012. The analysis reveals a small increase — only 2 percentage points since then, when 37% of non-retired adults ages 18 and older had done so.

Further analysis of changes in key population characteristics may help explain this limited progress. For example, the share of non-retired respondents with a retirement plan increased from 50% to 52%, and the share with household incomes above $50,000 rose from 46% to 55%. However, the share of respondents who correctly answered all three financial literacy questions declined over the same period, from 33% to 25%, potentially offsetting some of these gains.

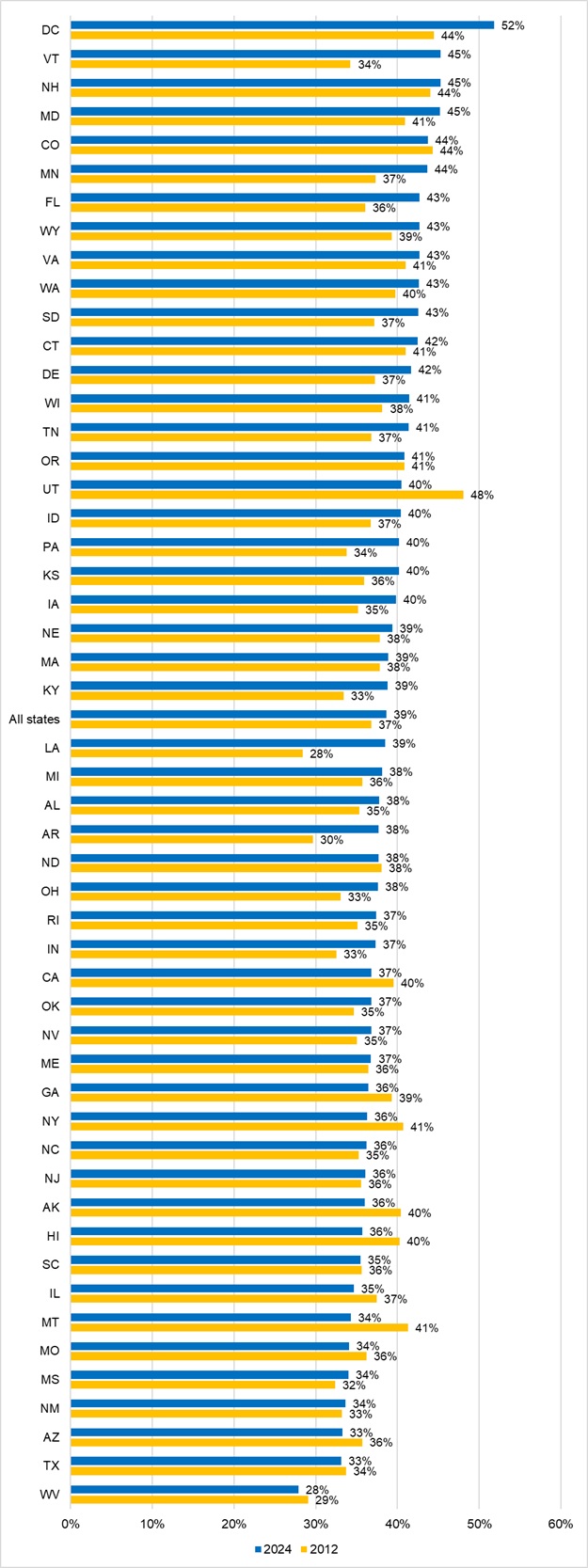

Retirement Planning Varies by State

The NFCS data also reveal significant differences among states in the share of non-retired adults who have estimated their retirement savings needs. At the high end, more than half of adults in the District of Columbia (52%) have done so. States such as Vermont, New Hampshire, and Maryland also report higher-than-average rates, exceeding 45%. In contrast, states such as West Virginia (28%) and Texas (33%) fall well below the national average, underscoring large geographic disparities in retirement savings planning engagement.

Share of Non-Retired Adults Ages 18+ Who Have Tried to Estimate Their Retirement Savings Needs by State (2012 & 2024)

Source: Authors’ calculations using the FINRA Foundation’s 2024 National Financial Capability Study, sorted from highest to lowest percentage in 2024.

Further analysis shows that there is a strong and significant correlation between the share of adults who have estimated their retirement savings needs and the share of adults in each state who: (1) have access to a retirement plan, (2) correctly answer three financial literacy questions, and (3) have household incomes above $50,000.

From 2012 to 2024, 32 states and D.C. experienced increases in the share of adults estimating their retirement savings needs, while 18 states saw declines or rates remaining unchanged. Notably, 13 reported positive changes of more than 5 percentage points, while three reported a negative change of more than 5 percentage points.

Conclusion — States Have Opportunities to Improve Retirement Readiness

The NFCS state-level data provide valuable insights for identifying differences in retirement planning across states and tracking changes over time. These findings highlight a gap between the behaviors of earning and saving and the equally important behavior of planning.

This gap suggests that teachable moments and opportunities, such as when people gain coverage, change jobs, or receive a pay raise, are not being fully seized. The findings also indicate that declines in financial literacy may be offsetting some of the positive effects of higher income and broader access to retirement plans.

States have levers to address these challenges through their efforts to expand financial education and retirement plan access. For example, state initiatives to expand retirement plan coverage, such as launching state-sponsored auto-IRA programs, can be leveraged to help close these gaps. As more workers gain access to retirement savings vehicles through these initiatives, savers can be supported better and encouraged to estimate and plan for their retirement needs.

Similarly, 30 states now require students to complete at least one semester of personal finance coursework to graduate from high school, and many other states are considering similar requirements. These efforts can provide foundational financial literacy that is needed for long-term savings and planning.

Together, these two policy levers not only create opportunities to enhance retirement planning today but may also have long-term effects as state-sponsored programs continue to expand and reach new enrollment milestones, and as the current generation of high school students who have taken financial literacy courses enters the labor force.

2025-05

Hector Ortiz, PhD, is a retirement and aging expert whose work focuses on debt, retirement planning, financial literacy and well-being, benefits access, and fraud prevention. He has held senior roles at the Consumer Financial Protection Bureau’s Office for Older Americans, U.S. Senate Special Committee on Aging, and National Council on Aging. This blog was written on his own time, without the use of taxpayer-funded resources, and does not necessarily represent the views of the Consumer Financial Protection Bureau.

Carly Urban, PhD, is a Professor of Economics in the Department of Agricultural Economics and Economics at Montana State University, a research fellow at the Institute for Labor Studies (IZA) and an academic fellow at the TIAA Institute. Her research focuses on financial education, literacy, and well-being across the life course.

Additional Resources

Employee Benefit Research Institute (EBRI), 2025 Retirement Confidence Survey.

FINRA Foundation, 2024 National Financial Capability Study (NFCS).