Here are several forward-looking ideas for defaults within the industry’s reach that can facilitate better outcomes by creating a path for current and future innovations.

By Jason Shapiro

Target-date funds, which have become a popular default investment in defined contribution (DC) retirement plans, are a great tool to help American workers prepare for retirement, but we feel they are not necessarily designed to serve the needs of today’s retirees who are living longer than those in the past.

U.S. employers and their workers have a lot riding on their DC plans: Four out of five organizations offer only DC plans to their new hires, making these plans the primary source of retirement income for many, according to our research.

At the same time, target-date funds have become the Qualified Default Investment Alternative (QDIA) of choice for nine out of 10 plans, and according to our research the vast majority of new entrants invest in them.

Target-date funds were designed as a cost-effective means to build retirement savings through a diversified portfolio that rebalances over time, but I think target-date funds don’t do well at addressing the competing objectives of participants crossing into retirement.

Some participants may stay in their plan after retirement and rely on target-date funds’ asset allocation for retirement income for 30 years or possibly even more. Others will roll their assets out of the plan to be invested elsewhere.

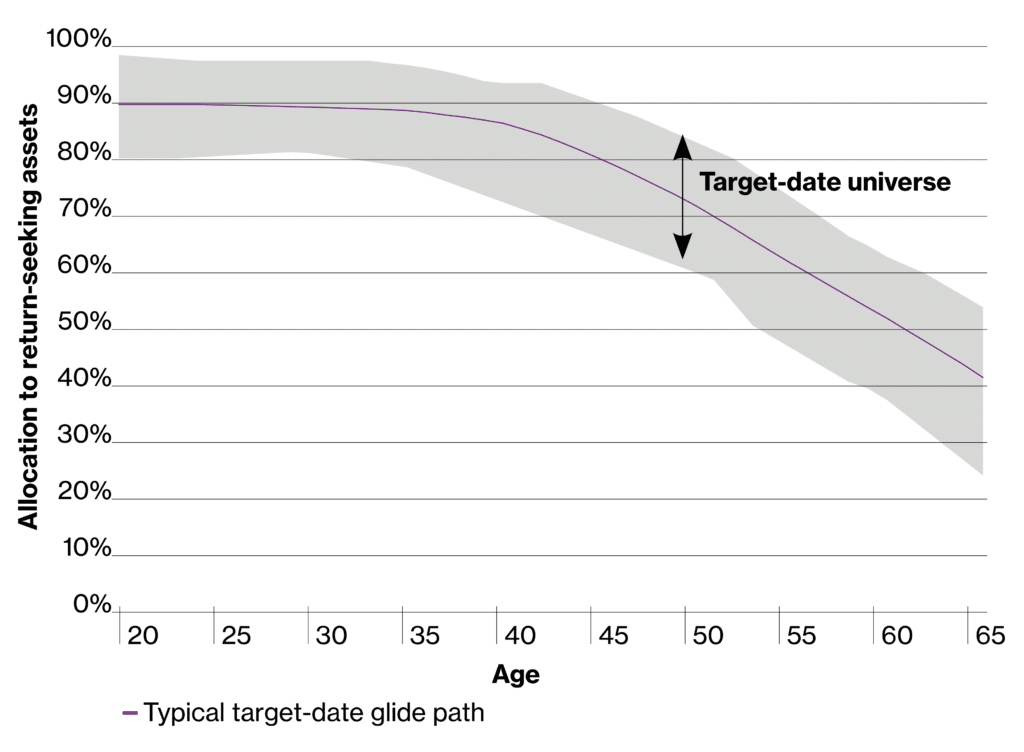

The first case calls for a strategy that combines income and growth — managing risk over time — such as a typical “through” glide path. The second suggests the glide path should significantly de-risk near retirement to protect the account balance for whatever next step participants have in mind, such as a typical “to” glide path. What matters more than the “to” versus “through” labels, however, is what the relevant risk level is at various points in participants’ life cycles.

Current target-date structures tend to manage these competing objectives through trade-offs. Sponsors are generally responsible for determining which target-date design makes sense for their participants, given demographics, behaviors, and fund objectives. This is a challenging task, and while the industry has developed most of the elements of a more-complete retirement solution, in my opinion, they have yet to broadly create more versatile and complete forms of QDIAs. On its own, change occurs slowly, so as an industry, we need to encourage progress by combining these existing components into more useful solutions.

The ‘Hybrid’ Model

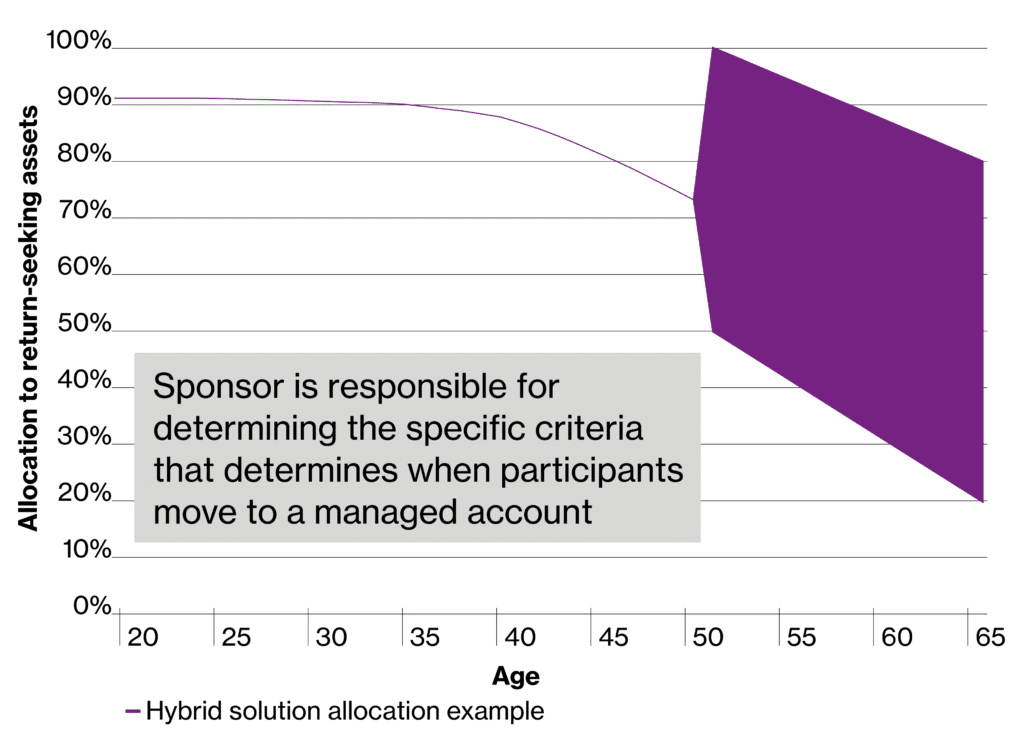

One development that has sprouted, dubbed a “hybrid QDIA” by its providers, delivers age-appropriate and individually customized portfolio allocations. A few recordkeepers have devised such arrangements, where a participant’s account is routed from the standard target-date fund to an individually managed account a few years before retirement. Thus, a participant gets personalized advice near and in retirement when it’s arguably most needed, but during the accumulation years, when most people are investing for growth and personalized allocations are likely to be less valuable, investors avoid the higher fees associated with managed accounts.

Figure 1 shows a stylized transition for someone at age 55 from a target-date glide path to the range of allocations that might be prescribed by the managed account provider.

Figure 1. Typical target-date glide path vs. hybrid solutions

Note: Sponsor is responsible for determining the specific criteria that determines when participants move to a managed account. For illustrative purposes only.

More Diversification

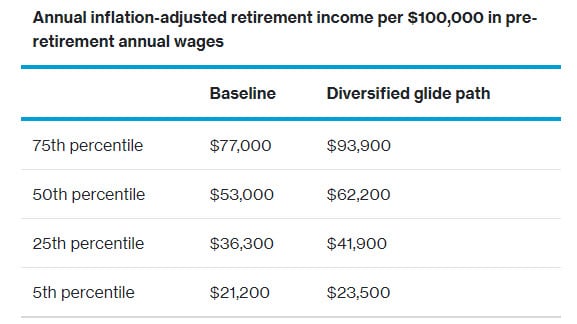

Another idea is a target-date fund with a more efficient investment design, going beyond stocks and bonds to a more diversified portfolio that includes less liquid assets. In 2018, my colleague David O’Meara and I partnered with the Georgetown University Center for Retirement Initiatives (CRI) to explore possible evolutions for target-date fund asset allocations and published a paper about the idea.

Through stochastic modeling of portfolios containing a diversified combination of direct real estate, private equity, and hedge funds, we found that expected risk was considerably reduced versus a baseline scenario, and median expected retirement income increased by 17%.

Figure 2 depicts the two portfolio strategies: The proxy target-date fund is heavy in public equities throughout, while the diversified glide path allocates decreasing proportions to public equities in the later years, replacing them with more diversified assets.

Figure 2: Distribution of potential retirement income for a full-career employee

Source: The Evolution of Target Date Funds: Using Alternatives to Improve Retirement Plan Outcomes, Georgetown Center for Retirement Initiatives, June 2018

This option offers significant potential improvements over current target-date funds, but will require a willingness on the part of investment solution providers to adopt some innovative methods to bring less-liquid private market assets into DC plans.

The ‘Unwrapped’ Model

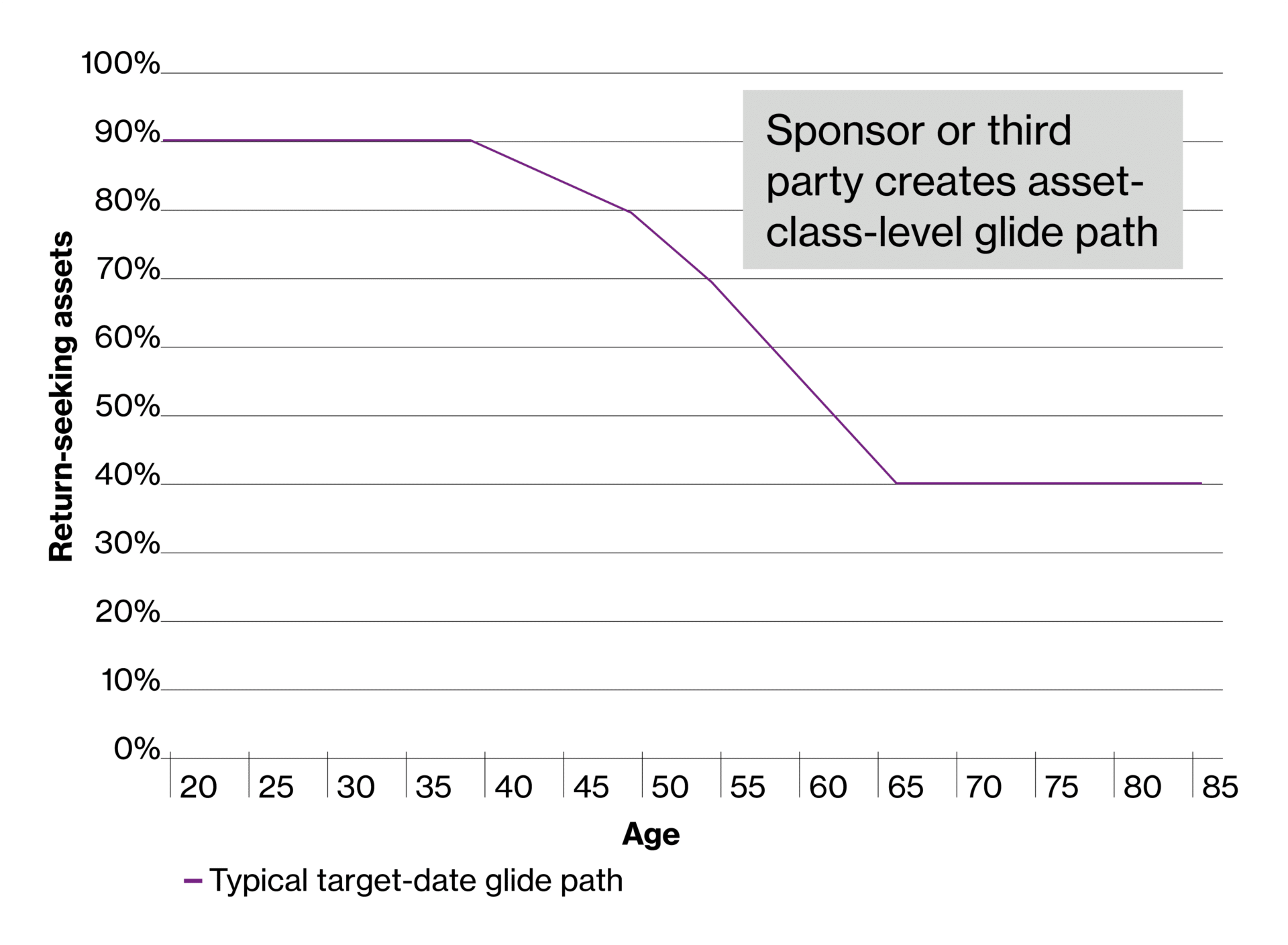

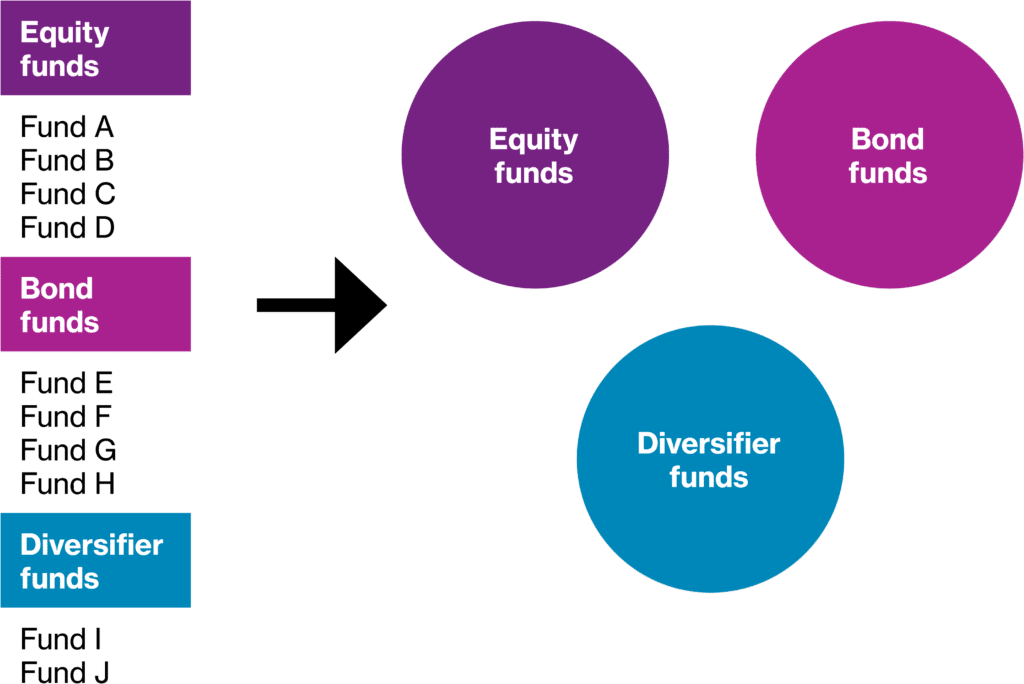

Another idea I like is an “unwrapped” target-date fund — a hybrid combining traditional model portfolios and custom target-date funds. A sponsor or advisor develops a series of model portfolios that suit the demographics and behaviors of its employee base. The model portfolios are assigned spots on a glide path, according to their risk levels and any other objectives (e.g. ability to generate income). They are invested in the plan’s core investment menu to benefit from asset scale. Non-core investments could be added as well, to create more diversified exposures.

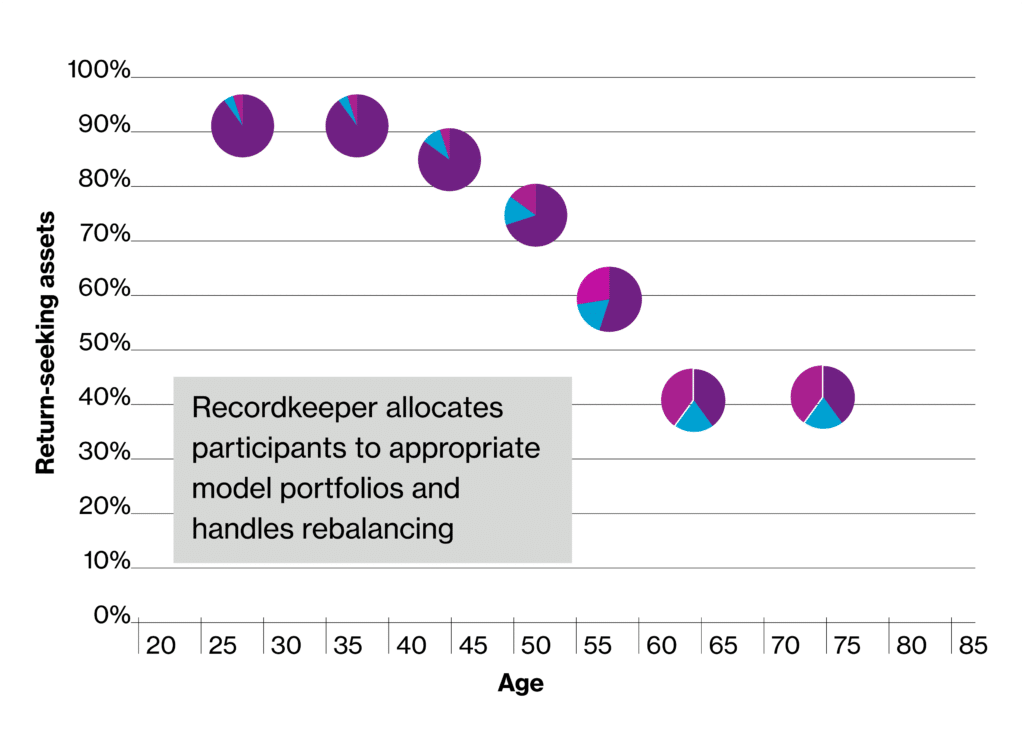

An unwrapped structure requires greater flexibility from a plan’s recordkeeper and places additional demands on fiduciary providers, but it may provide more advantages than the five- or 10-year vintages of typical target-date funds. It means that asset allocations ideally can track the glide path more closely (see Figure 3) while also providing potential operational and investment benefits. It also may be more cost-efficient than a traditional custom target-date structure.

Moreover, the flexible design lets the QDIA evolve as the sponsor wishes, allowing for the addition or refinement of retirement income options and distribution strategies. (A more-detailed discussion appears in our recent white paper, “QDIA evolutions — Moving defined contribution plans into the future”).

Figure 3. Unwrapped target-date fund schematic

Note: Sponsor or third party creates asset-class level glide path. For illustrative purposes only.

Figure 4. Core line up mapped to model portfolios to implement glide path

Note: Record keeper allocates participants to appropriate model portfolios and handles rebalancing. For illustrative purposes only.

Where Customization is Most Crucial

A separate — and accelerated — evolutionary track is needed for retirement income solutions in DC plans. This is where customization is most crucial, since participants’ retirement needs vary widely due to differences in asset levels, spending needs, and preferences. A QDIA designed to provide sustainable income can work much like a target-date fund or managed account, offering components for guaranteed income, dynamic spending, and coordination that manage tax liabilities and Social Security benefits.

Plan sponsors place many demands on target-date funds to meet the needs of a diverse population of plan participants. Some they fulfill quite well, such as providing professional asset allocation, helping reduce costs, and simplifying the participants’ experience. Other needs, particularly retirement income, are largely unmet. As an industry, we need to address the issue: Now is the time to design a full-featured QDIA to serve the waves of DC-dependent participants ready to move into retirement.

Jason Shapiro is a Director in Willis Towers Watson’s Investment practice and Head of QDIA Manager Research and Strategy.

A version of this blog post originally appeared on Willis Towers Watson’s website on November 21, 2019 and can be found here.

December 2019, 19-09

Additional Resources

Angela M. Antonelli, “The Evolution of Target Date Funds: Using Alternatives to Improve Retirement Plan Outcomes,” Center for Retirement Initiatives, McCourt School of Public Policy, Georgetown University and Willis Towers Watson, Policy Report 18-01, June 2018.

Angela M. Antonelli, “Generating and Protecting Retirement Income in Defined Contribution Plans: An Analysis of How Different Solutions Address Participant Needs,” Center for Retirement Initiatives, McCourt School of Public Policy, Georgetown University and Willis Towers Watson, Policy Report 19-02, June 2019.

Jason Shapiro, “QDIA evolutions — Moving defined contribution plans into the future,” Survey Report, Willis Towers Watson, April 29, 2019.

Willis Towers Watson, “Defined contribution retirement plans take center stage,” Survey Report, 2018.

Disclaimer

The information included in this presentation is intended for general educational purposes only and does not take into consideration individual circumstances. Such information should not be relied upon without further review with your Willis Towers Watson consultant. The views expressed herein are as of the date given. Material developments may occur subsequent to this presentation rendering it incomplete and inaccurate. Willis Towers Watson assumes no obligation to advise you of any such developments or to update the presentation to reflect such developments. The information included in this presentation is not based on the particular investment situation or requirements of any specific trust, plan, fiduciary, plan participant or beneficiary, endowment, or any other fund; any examples or illustrations used in this presentation are hypothetical. As such, this presentation should not be relied upon for investment or other financial decisions, and no such decisions should be taken on the basis of its contents without seeking specific advice. Willis Towers Watson does not intend for anything in this presentation to constitute “investment advice” within the meaning of 29 C.F.R. § 2510.3-21 to any employee benefit plan subject to the Employee Retirement Income Security Act and/or section 4975 of the Internal Revenue Code.

Willis Towers Watson is not a law, accounting or tax firm and this presentation should not be construed as the provision of legal, accounting or tax services or advice. Some of the information included in this presentation might involve the application of law; accordingly, we strongly recommend that audience members consult with their legal counsel and other professional advisors as appropriate to ensure that they are properly advised concerning such matters. In preparing this material we have relied upon data supplied to us by third parties. While reasonable care has been taken to gauge the reliability of this data, we provide no guarantee as to the accuracy or completeness of this data and Willis Towers Watson and its affiliates and their respective directors, officers and employees accept no responsibility and will not be liable for any errors or misrepresentations in the data made by any third party.

This document may not be reproduced or distributed to any other party, whether in whole or in part, without Willis Towers Watson’s prior written permission, except as may be required by law. In the absence of its express written permission to the contrary, Willis Towers Watson and its affiliates and their respective directors, officers and employees accept no responsibility and will not be liable for any consequences howsoever arising from any use of or reliance on the contents of this document including any opinions expressed herein. Views expressed by other Willis Towers Watson consultants or affiliates may differ from the information presented herein. Actual recommendations, investments or investment decisions made by Willis Towers Watson and its affiliates, whether for its own account or on behalf of others, may not necessarily reflect the views expressed herein. Investment decisions should always be made based on an investor’s specific financial needs.

Limitations of Analysis

In preparing the analysis contained in this report, Willis Towers Watson Investment (Willis Towers Watson) has used information and data provided to us by the Georgetown University Center for Retirement Initiatives. We have relied on all the data and information provided, including plan provisions and asset information, as being complete and accurate. We have not independently verified the accuracy or completeness of the data or information provided, but we have checked data for reasonableness to the extent that we believe appropriate based on the purpose for which it has been used.

The analysis contained in this report involves actuarial calculations. Actuarial calculations require that we make assumptions about future events. We have used assumptions that we believe are reasonable and appropriate for the purpose for which they have been used. Other assumptions may also be reasonable and could result in substantially different results.

In addition, because it is not possible or practical to model all aspects of a situation, we use summary information, estimates, or simplifications of calculations to facilitate the modeling of future events. We may also exclude factors or data that are immaterial in our judgment. We believe that we have not oversimplified the situation being modeled and have not inappropriately included or excluded any items.

Naturally, future events and actual experience will vary from the assumptions we have employed and calculations prepared with actual data will vary from estimates or summaries used for modeling purposes.

Because we use assumptions and estimates or summary information, actual future contributions or expense for accounting purposes may differ from our projections. As these differences arise, contributions or the expense for accounting purposes will be adjusted to take changes into account. These adjustments are anticipated in any actuarial calculations for ongoing entities. If these adjustments become material, they may result in the need for future adjustments to the valuation model.

The numbers in this report are not necessarily rounded. The use of unrounded numbers does not imply precision. Actuarial calculations are inherently imprecise.

The analysis reported has been prepared solely for the benefit of the Georgetown University Center for Retirement Initiatives. This report is not complete without the accompanying discussion with a representative of Willis Towers Watson. This report should not be used for purposes other than asset allocation strategy or relied upon by any other person without prior written consent.

Analysis in this report is based on the Willis Towers Watson Investment Model.

Services provided by Towers Watson Investment Services, Inc.