Portable Benefits and the Future of Retirement Access for Independent Workers

By Liya Palagashvili

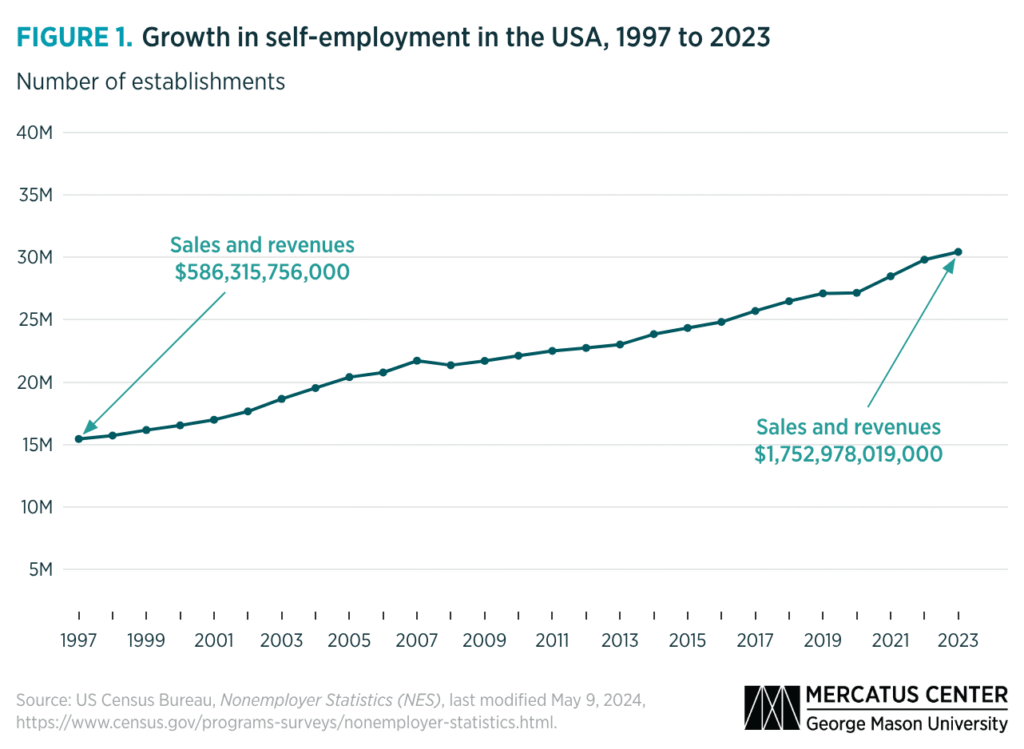

America’s workforce is undergoing a significant transformation. Across the country, more than 30 million people earn income — either as their main or secondary source — through freelancing, contracting, or self-employment, generating nearly $1.5 trillion in annual revenue, according to Census Bureau data.

Over the past decades, the number of Americans earning income outside traditional employment has surged, driven by technology, worker preferences, and evolving industry needs. Independent work now spans industries from professional services and real estate to transportation, construction, retail, health care, and finance.

This shift reflects the evolving nature of work in the United States, but the nation’s benefits system has not kept pace. Most benefits — such as health coverage and retirement contributions — remain tied to traditional employer-employee relationships, leaving independent workers to navigate fragmented and often expensive alternatives.

States across the country are responding with a solution that matches the modern workforce: portable benefits.

What Are Portable Benefits?

Portable benefits are worker-owned accounts that stay with the worker and are not connected to any single employer. Businesses or clients can voluntarily contribute to a worker’s benefit account, allowing benefits to follow workers among jobs, projects, or platforms.

According to the Bureau of Labor Statistics, about 80 percent of independent workers prefer to remain self-employed rather than transition (or return) to traditional employment. At the same time, surveys show that 81 percent of self-employed workers want access to portable benefits options that provide greater security without changing how they work.

Rather than attempting to reclassify independent workers as employees, a step that reduces work opportunities altogether, portable benefits offer a flexible and voluntary alternative for this growing workforce.

Retirement Coverage Gap for Independent Workers

While independent work has expanded economic opportunity, it has also exposed a weakness in the U.S. retirement system: Most retirement savings vehicles remain tied to traditional employer-sponsored plans.

Pew research finds that more than half of nontraditional workers lack access to a workplace retirement plan, and roughly two-thirds lack access to defined contribution plans — the primary retirement savings vehicle. The gap is even larger for workers whose primary income comes from nontraditional work arrangements: More than 70 percent lack access to a workplace retirement plan, and only 22 percent participated in a workplace defined contribution plan in the previous year.

These figures highlight a mismatch between a retirement system built around traditional payroll employment and a workforce where many workers earn income from multiple clients or projects.

Portable Benefits and State Auto IRA Programs

Over the past decade, 20 states have enacted state-facilitated retirement savings programs and 17 of these are automatic IRA programs, often referred to as auto-IRA programs. These initiatives automatically enroll employees in payroll-deduction IRAs when their employers do not offer workplace retirement plans.

While auto-IRA programs have broadened retirement access for workers at firms without retirement plans, they are largely designed around payroll-based employment relationships. As a result, many independent workers remain outside the reach of these systems.

Portable benefits frameworks can help bridge this gap. They may be especially valuable for the roughly 11.9 million Americans who rely on independent work as their primary job, according to the Bureau of Labor Statistics. Unlike supplemental earners with W-2 jobs, these workers often lack access to workplace retirement savings.

Under a voluntary portable benefits model, companies or clients could contribute to a worker-owned benefits account. The worker would then decide how to allocate those funds — including directing retirement contributions into an IRA such as a state auto-IRA account. Because these accounts are worker-owned and voluntary, this approach does not convert state auto-IRA programs into employer-sponsored plans or create new ERISA obligations. Instead, portable benefits accounts can serve as a flexible pathway for independent workers to connect to existing retirement systems.

Momentum in the States

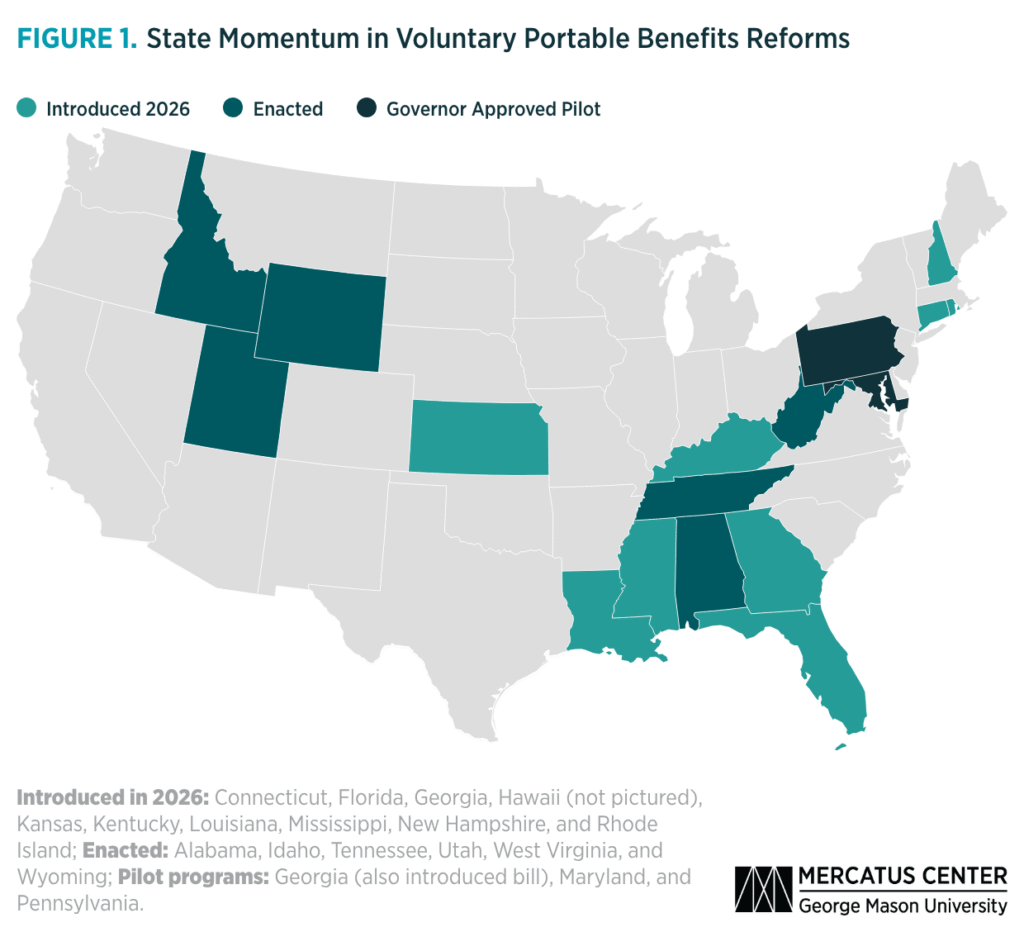

Interest in portable benefits is growing rapidly across the country. In the past two years, states including Alabama, Idaho, Tennessee, Utah, West Virginia, and Wyoming have enacted voluntary portable benefits framework, clarifying that businesses may contribute to independent workers’ benefit accounts without triggering employment reclassification. Several states — including Pennsylvania, Maryland, and Georgia — are also experimenting with pilot programs in partnership with DoorDash.

Legislative interest is also expanding rapidly. As of March 2026, lawmakers in Florida, Georgia, Kansas, Kentucky, Louisiana, Mississippi, New Hampshire, and Rhode Island have introduced legislation that includes a voluntary portable benefits safe harbor provision, allowing companies and clients to contribute to independent workers’ benefit accounts. Connecticut and Hawaii have introduced similar safe harbor language focused specifically on portable health benefit contributions.

Together, these developments reflect a broader shift among policymakers seeking flexible solutions that support independent workers while preserving the independence that many workers value.

Removing Legal Barriers to Voluntary Portable Benefits

As states explore ways to expand portable benefits, many are focusing on a simple but important policy change: clarifying that businesses may contribute to independent workers’ benefits without triggering worker reclassification disputes.

Under current labor rules, companies that voluntarily offer benefits to independent contractors may risk creating evidence that those workers should be classified as employees.

Portable benefits safe harbor laws are designed to address this challenge. These laws clarify that voluntary benefit contributions to independent workers should not be used as evidence of employment status. By removing this legal ambiguity, states can allow companies, clients, platforms, and other organizations to contribute to worker-owned benefit accounts without risking misclassification disputes.

A typical voluntary portable benefits framework includes three elements:

• Voluntary participation — Contributions are optional.

• Neutrality on worker status — Contributions do not affect classification.

• Worker ownership — Accounts follow workers across jobs.

By clarifying these rules, portable benefits frameworks create opportunities for new benefits models while preserving the flexibility that many independent workers value.

Conclusion: Expanding Security for Independent Workers

Portable benefits frameworks offer a pathway for independent workers to build financial security while maintaining the flexibility that defines modern work. By clarifying that businesses and clients may voluntarily contribute to worker-owned benefit accounts without triggering reclassification disputes, states can expand access to benefits — including retirement savings — while preserving that flexibility.

26-03

March 2026

Liya Palagashvili is a Senior Research Fellow and Director of the Labor Policy Project at the Mercatus Center at George Mason University. Her research focuses on labor regulations, the gig economy, and the changing nature of work.

Additional Resources

Palagashvili, Liya. (2025). “Bringing Portable Benefits to America’s Independent Workforce: Overview.” Mercatus Center at George Mason University.

Palagashvili, Liya, et al. (2024). “Assessing the Impact of Worker Reclassification: Employment Outcomes Post-California AB5.” Mercatus Working Paper, Mercatus Center at George Mason University.

Palagashvili, Liya. (2023). “Flexible Benefits for a Flexible Workforce: Unleashing Portable Benefits Solutions for Independent Workers and the Gig Economy.” Mercatus Policy Brief, Mercatus Center at George Mason University.