Retirement Savers and AI Advice: Who is Interested and How Can We Use It to Improve Financial Capability?

By Hector Ortiz, Ph.D.

The month of April is Financial Capability Month. Financial capability — the knowledge, skills, attitudes, and access to the products and services that enable people to manage money effectively — plays a critical role in the economic well-being of all Americans.

This month, as hundreds of organizations shine a bright light on the challenges and opportunities involved in strengthening financial capability, one important emerging theme is the growing use of artificial intelligence (AI) as a tool to support financial decision-making.

AI-powered tools provide access to conversational, interactive features that resemble financial coaches and planners. They can simplify the process of gathering information, generating content, and conducting mathematical computations by combining these tasks in a single tool.

When it comes to strengthening retirement security, AI could offer important opportunities to improve preparedness and financial literacy, as well as support positive financial behaviors. For example, AI tools may help users create action plans, provide a rough estimate of retirement income needs, develop checklists of important steps, and evaluate trade-offs among different decisions. Because retirement savers can often obtain access to this advice at no cost, AI may also help address attitudinal barriers, such as fear of being judged.

These opportunities, however, are not without risks and important considerations. AI systems rely on existing information, which may become outdated as policies change. Questions remain regarding accuracy, data security, and privacy of shared information. Lastly, in contrast to advice provided by humans and institutions, the systems to ensure accountability for the accuracy of information and advice remain unclear and are rapidly evolving.

Who Is Interested in Financial Advice from Artificial Intelligence?

What are the characteristics of retirement savers who express interest in using AI for financial decision-making and planning? To consider this, I examined data from the 2024 wave of the FINRA National Financial Capability Study (NFCS), which asked respondents for the first time whether they would be interested in receiving financial advice from AI.

While the survey does not specify whether the AI advice would come from a standalone tool or be powered by a financial institution, nor does it specify the domain of advice, it does provide other important information about people interested in receiving advice from AI tools. The survey asks whether respondents have employer-sponsored or non-employer retirement accounts, along with questions about a range of financial experiences. Together, these questions allow us to explore meaningful patterns in who is interested in AI advice.

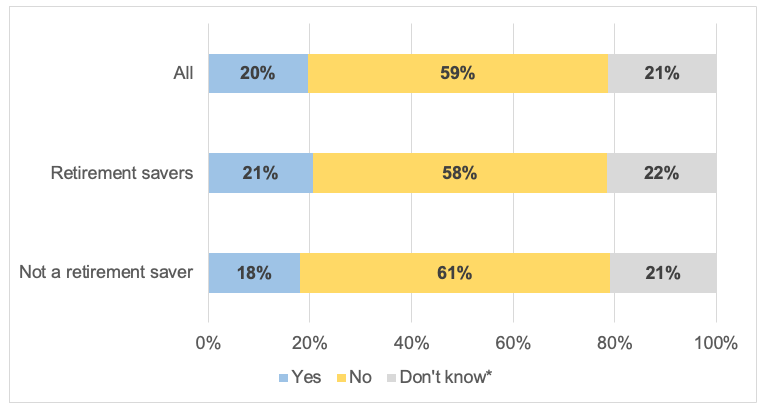

Approximately one respondent in five reported being interested in receiving financial advice from AI, with a slightly higher rate among retirement savers than non-savers (Figure 1). In comparison, for example, a recent KFF survey found that 32% have used AI to receive advice on health matters. At the same time, a similar share — also about one in five respondents — said “I don’t know.” This large proportion of uncertain responses reflects the early stages of artificial intelligence adoption. For example, the Pew Research Center finds a similarly sized share (about 20%) of respondents who are unsure about the use and value of AI advice for solving problems or making “difficult” decisions.

Figure 1: Percentage of Retirement Savers Interested in Receiving Financial Advice from Artificial Intelligence

Source: Author’s calculations using the FINRA Foundation 2024 National Financial Capability Study. *Don’t know includes the category “Prefer not to say.” Fewer than .05% of respondents selected this response.

Interest in AI Advice Varies Among Demographic Groups

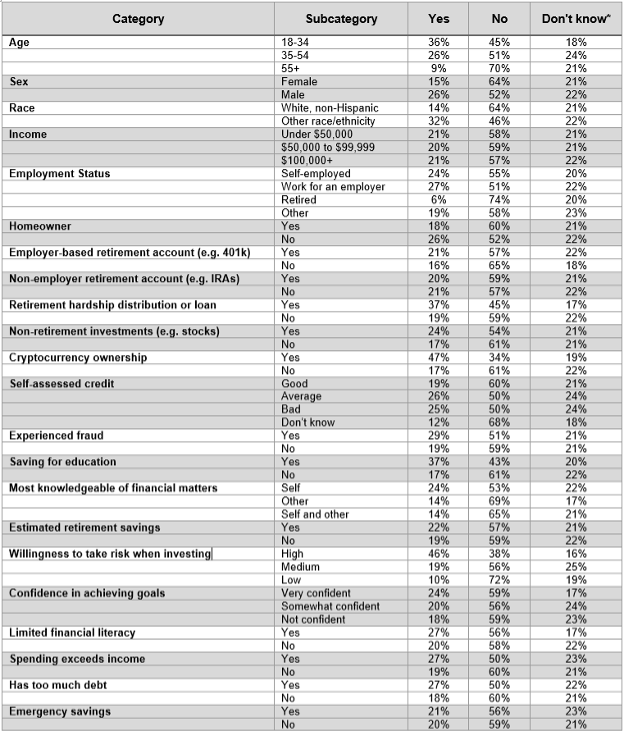

Interest in financial advice from AI varies considerably among key demographic groups. Among retirement savers, interest tends to be higher for younger respondents, men, non-white respondents, and non-homeowners (Figure 2).

These differences raise important questions. Is the AI advice aligned with the needs of these groups? Could these observed differences in interest by age, race, and sex eventually contribute to disparities in financial outcomes and access to support?

Figure 2: Percentage of Retirement Savers Interested in Receiving Advice from Artificial Intelligence by Selected Demographic and Financial Characteristics

Source: Author’s calculations using the FINRA Foundation 2024 National Financial Capability Study. *Don’t know includes the category “Prefer not to say.” Fewer than .05% of respondents selected this response.

Beyond basic demographic patterns, the analysis reveals several defining characteristics of retirement savers interested in AI advice.

- Employment and retirement plan type: Interest in AI advice is higher among those who are employed and those with employer-sponsored retirement plans rather than non-employer plans like IRAs.

- Greater risk exposure: Those interested in AI advice tend to have higher exposure to financial risk. They are more likely to own investments beyond traditional retirement accounts, including cryptocurrency. They report greater willingness to take financial risks and are more likely to have experienced fraud.

- Knowledge gaps: Interest in AI advice is also higher among those who show signs of financial knowledge gaps. For example, they were more likely to answer incorrectly or say they don’t know the answer to all three common questions about inflation, compound interest, and risk diversification.

- Financial vulnerability: Interest is higher among financially vulnerable individuals. These are the respondents more likely to report higher debt burdens, spending that exceeds income, and other indicators of financial strain. Interest is also particularly high among those who have taken loans and hardship distributions from their retirement accounts.

- No differences by income level: This may reflect the complex financial profile of those interested in AI, which — as noted here — includes younger adults, individuals with assets, and those exhibiting a wide range of financial vulnerabilities.

The Opportunities and Challenges of AI

This analysis provides important insights into the demographic and financial characteristics of retirement savers interested in AI advice. Notably, interest is higher among savers who are younger, non-white, employed, and already engaged with investment vehicles. At the same time, interest is also higher among those who report higher exposure to financial risks and face greater financial vulnerabilities, including accessing their retirement savings through loans or hardship distributions.

In summary, these findings suggest the retirement savers most interested in AI advice are those facing a complex financial profile and financial challenges, willing to take greater risk as a way to improve their financial situation, and for whom traditional human advice may be unavailable or unaffordable. AI could help with the latter: Financial professionals are already using AI to enhance their work through note-taking, synthesizing information, and follow-up communications. These efficiencies could lower the cost of providing advice, and allow advisors to focus on tasks that are uniquely suited for human interaction, such as those involving emotional and behavioral interventions. For financial institutions, AI also presents an opportunity to reach, at scale, individuals who currently receive no advice at all.

AI presents both significant opportunities and meaningful challenges in meeting these needs. On one hand, it has the potential to expand access to groups that may be priced out of human advice. On the other hand, these same groups may be more vulnerable to risky or inappropriate advice and less able to absorb financial losses.

These patterns suggest three priority areas for strengthening financial capability with AI tools and techniques.

- Building combined digital and financial literacy skills: teaching effective AI use, including how to write clear prompts and compare outputs among multiple tools, especially understanding differences between advice generated directly by publicly available AI tools and tools sponsored by financial institutions.

- Strengthening awareness of privacy and data security: supporting digital literacy and tool design that ensure users understand how their data might be used and the risks of information being lost or stolen.

- Understanding limitations and accountability: helping consumers understand the current limitations of AI tools and what to do when they encounter problematic guidance, including recognizing advice that appears unrealistic, misleading or incomplete.

On March 24, the U.S. Department of Labor launched an initiative to provide a free AI literacy course that addresses several of the areas identified above, including effective use, how to create effective and clear prompts, helping people assess AI-generated results for accuracy and relevance, and teaching them how to protect sensitive information.

As AI becomes increasingly integrated into financial decision-making, ensuring that individuals have the skills to use these tools effectively will be as important as expanding access to the tools themselves. This analysis highlights the importance of ensuring that AI tools providing financial advice are designed and governed in ways that support informed and secure decision-making. In the absence of these complementary safeguards, there is a risk that expanded access will come at the cost of greater risk for those who are already vulnerable.

2026-04

April 2026

Hector Ortiz, Ph.D., is a Non-Resident Scholar, Center for Retirement Initiatives (CRI), Georgetown University.

The views expressed in this blog and the paper are the author’s own and do not necessarily reflect the views of the CRI or any other institutions with which the author is affiliated. The author assumes full responsibility for any errors or omissions.

Additional Resources

FINRA Investor Education Foundation. (2025). Foundation’s National Financial Capability Study (6th ed.).

Michael Roberts. (2023). “Does Generative AI Solve the Financial Literacy Problem?” Knowledge at Wharton.

U.S. Department of Labor. (2026). Make America AI-Ready.

CPP Board. (2025). “Human + Machine: How AI Is Reshaping Financial Planning.”

Vanguard. (October 2025). “What AI can—and can’t—replace in financial advice.”