How Unequal Access to Employer-Sponsored Benefits Affects Worker Retention and Financial Stability

By Manita Rao and Jeremy Burke

Employers play a vital role in advancing employee financial wellbeing. Employer-provided health and retirement benefits are a primary means for workers to gain access healthcare services and prepare for retirement. Despite the importance of employer-sponsored benefits in helping workers meet their financial and healthcare needs, there are persistent inequities in access to employer-provided benefits. In our recent CRI working paper titled “Inequitable Access to Employer-Sponsored Benefits, Financial Stability, and Employee Turnover,” we document inequities in some of the most widely provided employer benefits. We then examine how inequitable access to employer-sponsored benefits affects employers and employees, using indicators of workplace productivity and financial stability.

Using data from the Understanding America Study covering 2021 to 2023, our analysis shows persistent (and in some cases, growing) gaps in access to employer-sponsored benefits across race and sex. We also find that employees without access to workplace benefits are more likely to be financially stressed, while those with such benefits — particularly employees who have access to paid leave, insurance, and flexible work arrangements — are more likely to be financially satisfied. Further, we find a strong correlation between reduced employee turnover and access to paid leave and work from home benefits.

Overall, our findings support the need for expanding coverage of employer-provided benefits to all workers and extending the range of benefits beyond traditional benefits like employer-provided health insurance and employer-sponsored retirement plans. New age benefits such as paid leave and work from home can increase productivity by improving financial wellbeing for employees and reducing turnover costs for employers.

Benefit Costs Have Increased but Differences in Access Remain

Workplace benefits constitute a significant proportion of compensation. In 2022, benefits constituted 31.2 percent of total compensation. Benefits for workers in the 90th percentile of the household income distribution were 79 percent higher than for workers at the 10th percentile (per the Department of Labor). In addition, while benefit costs have increased over time, these increases were larger for benefits provided to higher-income groups. Between 2013 and 2022, benefit costs for employees in the 90th percentile of the income distribution rose by 35 percent, compared to 32 percent for workers in the 10th percentile.

Access to traditional benefits such as employer-provided health insurance and employer-sponsored retirement plans vary by benefit type, occupational group, and firm size. In 2022, medical care and health insurance benefits were available to 72 percent of private sector workers, but only 43 percent had access to dental benefits and 28 percent had access to vision benefits (Department of Labor, 2022). While 94 percent of workers in management, business, and financial occupations had access to medical care benefits, only 52 percent of workers in service occupations had access to these benefits. Similarly, only 56 percent of workers in establishments with fewer than 50 workers had access to medical care benefits compared to more than 91 percent for workers in establishments with 500 workers or more.

Similarly, nearly 75 percent of private sector workers had access to retirement benefits in 2022, but access was distributed inequitably. More than 90 percent of workers in the management, business, and finance occupations had access to these benefits, compared to only 47 percent of workers in service occupations. Additionally, 93 percent of workers in the highest 10th percentile of the wage distribution had access to retirement benefits, yet only 52 percent of workers in the bottom 25th percentile had access to these benefits. Access to retirement benefits is also higher for employees of larger firms (90 percent) compared to smaller firms with fewer than 100 employees (58 percent).

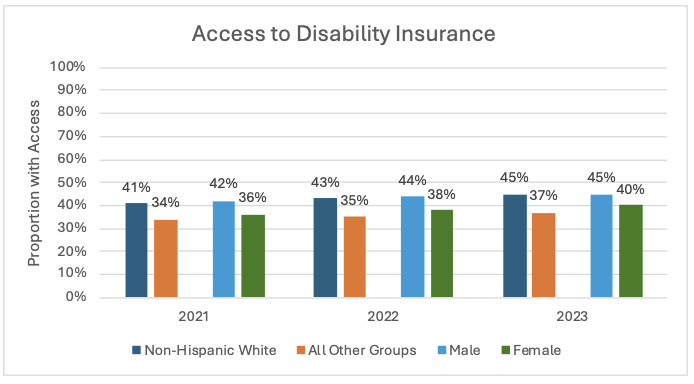

Inequities in Workplace Benefit Access by Race and Gender

While there are disparities in access to benefits for race and gender groups, there is limited research about such disparities by benefit type. Our analysis, using data from the Understanding America Study, looks at how access to employer-provided benefits varies by race and gender. The charts in the panels below show disparities in access by race and gender, for six types of employer-provided benefits — health insurance, retirement plans, paid sick leave, work-from-home, life insurance, and disability insurance — for 2021, 2022, and 2023.

Among all types of benefits, we observe higher access among Non-Hispanic white adults and males compared to females and all other groups. For example, in 2023, there’s a 6-percentage point difference in access to retirement accounts between Non-Hispanic white and other racial groups and a 4-percentage point difference between males and females. Similarly, there is an 8-percentage point difference in access to disability insurance between Non-Hispanic white and other racial groups and a 5-percentage point difference between males and females.

Employer-Sponsored Benefits and Employee Financial Stability

Do employer benefits influence employees’ financial security? We examined two indicators of household financial security: financial satisfaction and financial stress. We found that access to employer-sponsored life insurance, disability insurance, and an ability to work from home are all statistically significantly linked to high levels of financial satisfaction. For example, as shown in the left-hand panel of the figure below, individuals who work for employers that provide life insurance benefits are 3.3 percentage points more likely to be highly financially satisfied — a 9.5 percent increase relative to the sample mean.

The right-hand panel in the table below shows that paid vacation or sick leave; access to a defined contribution plan; and access to life and disability insurance are all statistically significantly associated with a lower likelihood of being financially stressed. For example, those working for an employer providing paid leave are 3.7 percentage points less likely to report “high” or “moderate” amounts of stress due to their financial situation (an 11.1% reduction relative to the sample mean).

Employer-Sponsored Benefits and Employee Turnover

To examine how access to employer-sponsored benefits affect employee turnover, the working paper leverages questions in the 2022 and 2023 surveys to elicit whether respondents changed employers over the last 12 months. Leveraging these data, it examines how benefit access in 2021 and 2022 influenced whether an individual changed employers in the next year. Approximately 9 percent of individuals changed employers in 2022 and 2023. Findings presented in the figure below show that nearly all benefits examined are at least directionally associated with lower employee turnover. Two of the estimated associations are statistically significant: Paid vacation or sick leave and an ability to work from home are associated with a 2.3–2.4 percentage point reduction in the likelihood of leaving one’s employer in the next year, corresponding to an approximate 25% reduction in the sample mean turnover.

Conclusion: Reducing Inequities in Benefit Access is Financially Advantageous to Employees and Employers

Employers are uniquely positioned to help their employees secure financial stability. Beyond wages, employers also frequently provide benefits, such as paid time off and health insurance, that can play an important role in helping individuals cope with life shocks and financial emergencies. Using longitudinal data from a nationally representative internet panel to examine the evolution of racial and gender gaps in access to employer-sponsored benefits over the 2021 to 2023 period and explore how benefits relate to financial security, we find substantial, persistent, and in some cases, growing differences in access to benefits between non-Hispanic white adults and males than those in other groups and females.

Importantly, the analyses of the relationship between employer-sponsored benefits and employee financial security underscore that these racial/ethnic and sex disparities matter. The findings show that access to employer-sponsored benefits increases financial security and that such benefits are systematically linked to higher financial satisfaction and lower financial stress.

The findings also present evidence that benefit provision can help employers directly; all of the benefits examined are at least directionally associated with lower employee turnover and two benefits — paid leave and work-from-home — are associated with reducing turnover by as much as 25 percent.

Taken together, our findings suggest that persistent, inequitable access to employer-sponsored benefits may be contributing to the well-known gaps in financial security across race and sex. Importantly, the findings reveal that increased provision of benefits might not only reduce disparities in financial stability but also improve employer outcomes by reducing employee turnover.

2025-07

Manita Rao is a Senior Policy Advisor, Public Policy Institute, AARP, and a Non-Resident Scholar, Georgetown University Center for Retirement Initiatives

Jeremy Burke is a Senior Economist, Center for Social and Economic Research, University of Southern California

Additional Resources

Bloomfield, A., Cyronek, T., & Makridis, C. 2025. “Decomposing Historical Changes in Employer Costs and Contributions to Inequality.” Available at SSRN.

Department of Labor. 2022. “Employer Costs for Employee Compensation,” Bureau of Labor Statistics News Release USDL-22-1176