State Programs 2026: Partnerships Expand, More Programs Launch, and the Focus Will Be the Enactment of More New State Programs and Initiatives

2026 STATE PROGRAM STATUS

Since 2012, 49 states and the District of Columbia have acted to implement a new program, study program options, or consider legislation to establish state-facilitated retirement savings programs.

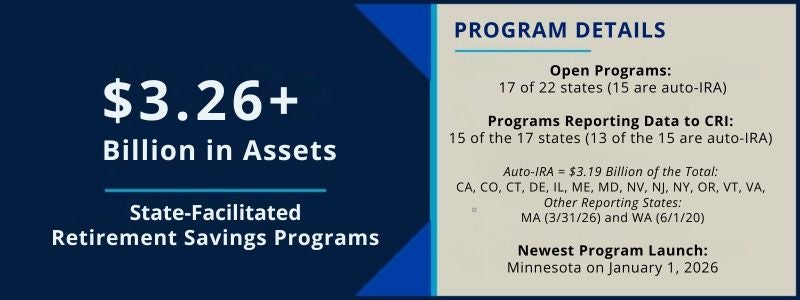

As of June 1, 2026, there are 22 states that have enacted new programs for private sector workers (and 3 cities for a total of 25 programs). New York City and Seattle will not move forward to implement due to state legal and program actions, but Philadelphia’s is expected to be implemented. 17 of these states are auto-IRA program states (and the 3 city programs are also auto-IRAs).

As of June 1, 2026, 17 of the 22 state programs — 15 auto-IRA (CA, CO, CT, DE, IL, ME, MD, MN, NJ, NV, NY, OR, RI, VT, VA) and 2 others (MA [MEP] and WA [Marketplace]) — are fully open to all eligible employers and workers. On January 1, 2026, the Minnesota auto-IRA program became the most recent program to open to all eligible employers and workers. On March 24, 2026, Utah enacted the first new program of 2026 (and the 21st state program) with the enactment of the new Utah Retirement Exchange. On April 8, 2026, Mississippi became the second new state program of 2026 (and the 22nd state program) with the enactment of the Mississippi Work and Save Program. On May 19, 2026, Philadelphia became the first new city program of 2026 (and the 3rd city program) with the creation of the Philadelphia Retirement Savings Board.

During the 2026 state legislative sessions to date, numerous bills to establish or amend state-facilitated retirement savings programs are being considered. As of June 2026, two states – New Jersey and Virginia – have passed legislation to amend their programs, including lowering their covered employer thresholds. In addition, two new state programs and one city program have been enacted: a retirement exchange in Utah, a voluntary payroll deduction IRA in Mississippi, and an auto-IRA program in Philadelphia. See the map below tracking the status of state program implementations around the country and the states that have active program or study bills (green color). Login required to view bill tracking and program updates.

Below are some of the 2026 legislative highlights so far:

- On January 20, 2026, a New Jersey law amending the NJ Secure Choice Savings Program was enacted. The threshold for required participation was lowered from 25 to 10 employees.

- On April 6, 2026, Virginia’s governor signed a bill reducing the threshold for employer eligibility from 25 to five employees. The law also removes the prior restriction on “eligible employees” to those working at least 30 hours per week.

- On June 23, 2026, Rhode Island’s governor signed into law several technical amendments to the RI Secure Choice Retirement Savings Program. Under this legislation, investments must be reviewed at least every three years. The law also defines an “optional employee” as an adult whose employer is ineligible, but who opts to enroll in the program.

In 2025, although no new programs were enacted, several states successfully amended their existing programs, including Connecticut, Hawai’i, Illinois, Maryland, Massachusetts and Minnesota. Notably, Hawai’i enacted legislation to switch from an opt-in model to an opt-out, automatic enrollment model, and Massachusetts raised the cap on its MEP program from employers with a maximum of 20 employees to employers with at most 100 employees.

2026 STATE LEGISLATIVE ACTION

Visit the CRI Supporters Homepage to access the 2026 state legislative map, detailed information on the progress of state program implementations, the State Resource Center and much more.

On March 24, 2026, Utah enacted the first new program of 2026 (and the 21st state program) with the enactment of the new Utah Retirement Exchange. On April 8, 2026, Mississippi became the second new state program of 2026 (and the 22nd state program) with the enactment of the Mississippi Work and Save Program. On May 19, 2026, Philadelphia became the first new city program of 2026 (and the 3rd city program) when voters approved the creation of the Philadelphia Retirement Savings Board via ballot measure.

2026 State Program Information Map

Click on this map to view quick links for program states

Click here to view 2026 map with detailed state legislative activity updates (login required)

© Copyright 2026, Georgetown University

Source: Georgetown University’s Center for Retirement Initiatives

Source: Georgetown University’s Center for Retirement Initiatives

Auto-IRA Active

Auto-IRA Adopted

Voluntary MEP, IRA or Marketplace Active

Voluntary MEP, IRA or Marketplace Adopted

★

Philadelphia City Auto-IRA

Legislation Introduced

Past Legislative Efforts

No Past Legislative Efforts

2026 STATE PROGRAM IMPLEMENTATION UPDATES

25 Programs (22 states and 3 cities)

There are now 25 enacted retirement savings programs (22 states and 3 cities**) for private sector workers.

To date, new programs have adopted one or a combination of these four models:

- Auto-IRA (employer participation required if no plan is already offered) – all other state programs and Philadelphia (see chart below)

- Payroll deduction IRA (voluntary) – MS and NM

- Multiple Employer Plan (MEP) (voluntary) – MA and MO

- Marketplace/Exchange (voluntary) – NM and UT

As of June 1, 2026, 17 of the 22 state programs — 15 auto-IRA (CA, CO, CT, DE, IL, ME, MD, MN, NJ, NV, NY, OR, RI, VT, VA) and 2 others (MA [MEP] and WA [Marketplace]) — are fully open to all eligible employers and workers. On January 1, 2026, the Minnesota auto-IRA program became the most recent program to open to all eligible employers and workers. On March 24, 2026, Utah enacted the first new program of 2026 with the enactment of the new Utah Retirement Exchange. On April 8, 2026, Mississippi became the second new enacted state program of 2026 with the Mississippi Work and Save Program. On May 19, 2026, Philadelphia became the first new city program of 2026 (and the 3rd city program) when voters approved the creation of the Philadelphia Retirement Savings Board via ballot measure.

| Individual Retirement Account (Auto-IRA) |

Voluntary Payroll Deduction IRA | Voluntary Marketplace | Voluntary Open Multiple Employer Plan (MEP) |

|

California |

Mississippi New Mexico**** |

New Mexico Utah Washington (active) |

Massachusetts (active) Missouri |

**New York City’s program will no longer be implemented because New York State enacted an auto-IRA program and New York City would now become part of the state program. The Seattle, WA program also has now become part of the new WA Saves state program.

***Washington enacted a new auto-IRA program in March 2024, but it is not scheduled to launch until July 2027. Because WA already has a voluntary marketplace and it remains in place, the enactment of the new auto-IRA program does not increase the number of states with programs.

****The New Mexico Work and $ave IRA Program was scheduled to be implemented on or before July 1, 2024, but has since been placed on an indefinite hold with no known new implementation date.

For an overview of all the state programs (with hyperlinks to state program websites and additional information), see State-Facilitated Retirement Savings Programs: A Snapshot of Plan Design Features (23-03, June 30, 2023 UPDATE).

PROGRAM LAUNCH AND EMPLOYER TIMELINES

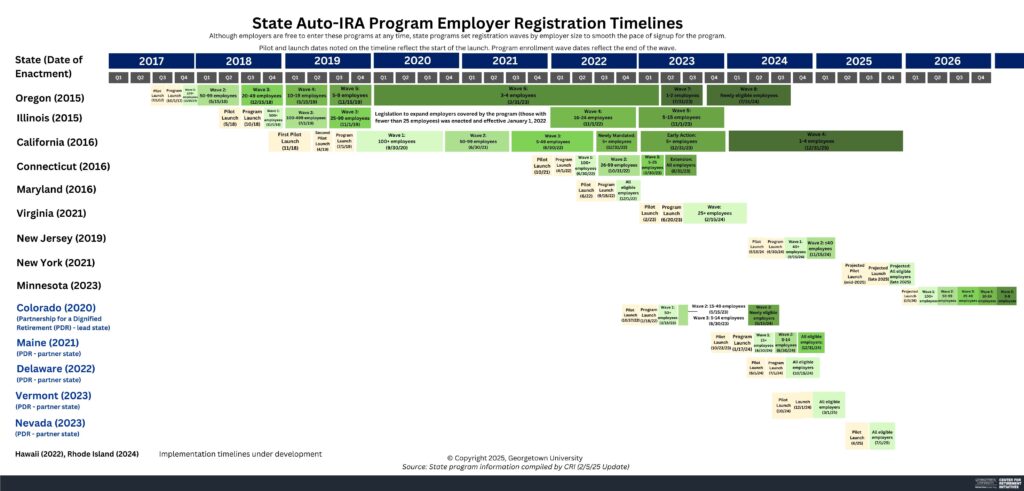

The lessons from older auto-IRA programs (i.e., OR, IL, and CA) suggest that state programs can shorten their timelines for onboarding employers. Also, the creation of new inter-state partnerships supports shorter launch and onboarding timelines, as illustrated by several of Colorado’s partner states, including Maine, Delaware, Vermont and Nevada.

Auto-IRA programs:

California: CalSavers launched its pilot program in November 2018 and statewide enrollment began on July 1, 2019. Registration was initially implemented in three waves: Wave 1 with employers with 100 or more employees required to register by September 30, 2020; Wave 2 with employers with 50 or more employees required to register by June 30, 2021; and Wave 3 with employers with 5 or more employees required to register by June 30, 2022. There was a wave for employers that had not yet received a registration notice, who were required to register by December 31, 2023. The final wave, for employers with 1-4 employees, closed on December 31, 2025.

Colorado: The Colorado Secure Savings Program launched its pilot program on October 17, 2022 and statewide enrollment began in January 18, 2023 in three waves: Wave 1 with employers with 50+ employees required to register by March 15, 2023; Wave 2 with employers with 15-49 employees required to register by May 15, 2023; and Wave 3 with employers with 5-14 employees, to register by June 30, 2023. Each year, businesses that are newly eligible as of April are required to register by May 15th of that year.

Connecticut: MyCTSavings launched its employer pilot program on October 25, 2021 and opened to all eligible employers on April 1, 2022 in three waves: Wave 1 with employers with 100 or more employees required to register by June 30, 2022; Wave 2 with employers with 26-99 employees required to register by October 31, 2022; and Wave 3 with employers with 5-25 employees required to register by March 30, 2023. The program deadline for all employers was extended to August 31, 2023. Following the three planned waves, newly eligible businesses were required to register by August 3, 2024.

Delaware: The DE EARNS pilot program for employers launched on May 1, 2024. The full program opened to all eligible employers on July 1, 2024. Employers were required to register by October 15, 2024. Newly eligible businesses were then required to register by June 30, 2025.

Hawaii: The state program is now part of the Connecticut Multistate Alliance for Retirement Security, joining with Rhode Island, and the program is expected to launch sometime in late 2026 or early 2027.

Illinois: Illinois Secure Choice, which was rebranded as My Illinois Savings in June 2026, launched its pilot program in May 2018. Statewide enrollment opened to all eligible employers in October 2018 in three initial registration waves: Wave 1 with employers with more than 500 employees required to register by November 2018; Wave 2 with employers with 100-499 employees required to register by July 2019; and Wave 3 with employers with 25-99 employees required to register by November 2019. In 2021, with the statutory lowering of the threshold from 25 to 5 employees, two additional employer registration waves were added: Wave 4 with employers with 16–24 employees required to register by November 1, 2022; and Wave 5 with employers with 5–15 employees required to register by November 1, 2023. Each year from 2024 forward, the program has an annual employer onboarding wave comprising newly eligible employers.

Maine: The Maine Retirement Investment Trust (MERIT) opened its pilot program for employers and employees on October 23, 2023. The full program launch, open to all eligible employers, began on January 27, 2024 in three waves: Wave 1 with employers with 15 or more employees required to register by April 30, 2024; Wave 2 with employers with less than 15 employees required to register by June 30, 2024; and Wave 3 with all remaining covered employers required to register by December 31, 2024.

Maryland: MarylandSaves launched its pilot in March 2022 and the full program launched on September 15, 2022. Employers were required to register by December 1, 2022.

Minnesota: The Minnesota Secure Choice Retirement Program opened on January 1, 2026 and will soft launch for any sized covered employer from January 1, 2026 – March 30, 2026. The full program launch will begin on April 1, 2026 in five waves: Wave 1 with employers with 100 or more employees required to register by June 30, 2026; Wave 2 with employers with 50-99 employees required to register by December 1, 2026; Wave 3 with employers with 25-49 employees required to register by June 30, 2027; Wave 4 with employers with 10-24 employees required to register by December 31, 2027; Wave 5 with employers with 5-9 employees required to register by June 30, 2028.

Nevada: The Nevada Employee Savings Trust (NEST) opened to all eligible employers on June 9, 2025. All employers were required to register by September 1, 2025.

New Jersey: The New Jersey Secure Choice Savings program, branded as RetireReady NJ, launched its pilot program in May 2024 and opened to all eligible employers on June 30, 2024 in two registration waves: Wave 1 with employers with 40 or more employees required to register by September 15, 2024; and Wave 2 with employers with 25-39 employees required to register by November 15, 2024.

New York: New York Secure Choice launched its pilot program on July 14, 2025. The full program opened to all eligible employers on October 8, 2025. There are three registration deadline waves: Wave 1 with employers with 30 or more employees required to register by March 18, 2026; Wave 2 with employers with 15-29 employees required to register by May 15, 2026; Wave 3 with employers with 10-14 employees required to register by July 15, 2026.

Oregon: OregonSaves launched its pilot on July 1, 2017. Statewide enrollment opened to all eligible employers on October 1, 2017 in seven registration waves: Wave 1 with employers with 100+ employees required to register by November 15, 2017; Wave 2 with employers with 50-99 employees required to register by May 15, 2018; Wave 3 with employers with 20-49 employees required to register by December 15, 2018; Wave 4 with employers with 10-19 employees required to register by May 15, 2019; Wave 5 with employers with 5-9 employees required to register by November 11, 2019; Wave 6 with employers with 3-4 employees required to register by March 1, 2023; and Wave 7 with employers with 1-2 employees or using a Professional Employer Organization (PEO) or Leasing Agency required to register by July 31, 2023. Each year, newly eligible employers are required to register by July 31st of the next year.

Philadelphia: On May 19, 2026, Philadelphia voters approved a ballot measure to create the Philadelphia Retirement Savings Board, which will implement an auto-IRA program in the city. By July 1, 2027, individuals will be able to begin making contributions to the plan.

Rhode Island: On September 24, 2025, the state announced the completion of its partnership agreement with Connecticut. The program opened on October 21, 2025, with three registration waves: Wave 1 with employers with 100 or more employees required to register by October 21, 2026; Wave 2 with employers with 50 or more employees required to register by October 21, 2027; Wave 3 with employers with 5 or more employees required to register by October 21, 2028.

Vermont: Vermont Saves launched its pilot program in October 2024. The program opened to all eligible employers on December 1, 2024. Employers were required to register by March 1, 2025. In February 2026, the program amended its rules to cover employers with 2 or more employees.

Virginia: The RetirePathVA retirement savings program facilitated by the Commonwealth Savers opened its pilot program on February 23, 2023, and the program opened to all eligible employers on June 20, 2023. All employers were required to register by February 15, 2024. On April 6, 2026, the governor signed into law program amendments effective July 1, 2026 that include lower the covered employer threshold from 25 to 5; remove the 30-hour week requirement for covered employees; establish the minimum covered employee age at 18; and expand the powers and duties of the governing board.

Washington: According to the legislation, Washington Saves must be launched by July 1, 2027 and current timeline targets a pilot on or about April 2027 with full launch by July 2027.

Other State Programs: The Massachusetts’ CORE MEP opened for enrollment in October 2017, and the Washington State Retirement Marketplace opened in March 2018. According to the legislation, the Missouri MEP plan should launch by September 1, 2025, but no official implementation schedule has been released. The New Mexico Retirement Plan Marketplace and the New Mexico Work and $ave IRA Program had a July 1, 2024 implementation deadline, but the implementation date has since been delayed with no new date set. The Utah Retirement Plan Exchange was enacted on March 24, 2026. The law states that the exchange platform should be set up no later than November 2, 2026 and begin accepting applications from plan providers. The Mississippi Work and Save Program was enacted April 8, 2026. The law states that individuals can begin contributing no later than August 1, 2028, with phased in implementation substantially completed no later than July 1, 2028.

State Partnerships: To date, 8 of the 17 auto-IRA programs have entered partnership agreements, and there are two distinct partnership arrangements.

In 2023, Colorado established the first partnership, creating the Colorado Partnership for a Dignified Retirement (PDR), and it has the following member states as of January 1, 2026 (in order of entrance): Maine, Delaware, Vermont, Nevada and Minnesota.

The second partnership arrangement, the Multistate Alliance for Retirement Security, was established in 2024 when Rhode Island announced its intent to partner with the already established MyCTSavings Program (Connecticut).

Colorado Partnership for a Dignified Retirement Timeline

- On December 2, 2025, the Minnesota Secure Choice Retirement Program and the Colorado Secure Savings Program finalized their partnership, making Minnesota the sixth state to join the Partnership for a Dignified Retirement (View press release). The Minnesota Secure Choice Retirement Program had announced on June 17, 2025 its intent to enter the Colorado Partnership for a Dignified Retirement.

- On December 17, 2024, the Nevada Employee Savings Trust (NEST) announced its intent to enter the Colorado Partnership for a Dignified Retirement. On April 30, 2025, Colorado officially announced that Nevada had entered the Partnership for a Dignified Retirement (View press release).

- On June 26, 2024, the Colorado Secure Savings Program and Vermont Saves announced a partnership (View press release).

- On December 7, 2023, the Delaware EARNS board approved negotiating a final partnership agreement with the Colorado Partnership for a Dignified Retirement (View press release).

- In June 2023, the Colorado Secure Savings Program and the Maine Retirement Investment Trust agreed to finalize the details of an interstate partnership, which was officially announced on August 15, 2023 (View press release).

- In November 2021, the Colorado Secure Savings Program and the New Mexico Work and $ave Program signed a first-in-the-country Memorandum of Cooperation (MoC) to pursue a formalized partnership agreement for their auto-enroll IRA programs. The MoC highlights areas of collaboration including shared program administration and financial services, marketing and outreach support, program evaluation and research, as well as data collection and participant privacy. As of January 2026, the Colorado and New Mexico partnership is currently on hold pending additional potential modifications to the design of the New Mexico state program.

Multistate Alliance for Retirement Security Timeline

- On February 10, 2026, the Hawaii Retirement Savings Board voted to enter the Multistate Alliance for Retirement Security.

- On October 21, 2025, the RISavers program opened to all eligible employers. Read the announcement.

- On September 24, 2025, Connecticut and Rhode Island announced the finalization of their partnership agreement that will now support the launch the new RISavers program.

- On November 20, 2024, Rhode Island Treasurer announced the intent of the Rhode Island Savers Program to partner with the MyCTSavings Program (View press release).